Common Mistakes Made in ICSE Class 10 Board Exams - Chapter Goods and Services Tax

Chapter Overview

GST is an indirect tax introduced by the Government of India from 1st July 2017.

- GST is a consumption based tax which is levied when one buys/transfers goods or services or both.

- GST is to be levied at every point of sale/transfer of goods or services or both.

- GST has replaced all former indirect taxes levied by central and state governments.

- GST is applicable throughout India.

Types:

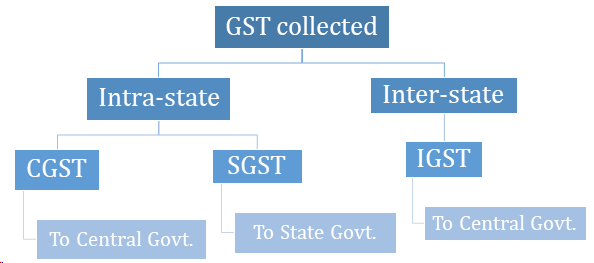

- Central-GST (CGST) is collected by the central government for the intra-state transaction or movement of goods and services within the state. In case of CGST, the beneficiary is the central government.

- State-GST (SGST)/Union territory GST (UGST) which is collected by the state government/union territory for the intra-state/union territory transaction or movement of goods and services. Whereas UGST the beneficiary is the union territory government.

- Integrated-GST (IGST) which is levied by the central government for inter-state transaction or movement (including imports) of goods and services.

Important Terms:

- Intra-state: supply within the same state.

- Inter-state: supply from one state to another state.

Remember:

- GST is a destination based consumption tax.

- A consumer (end user) cannot claim the GST paid by him.

- Only a person or an organization registered with GST can charge and collect GST on sale/transfer of goods and services.

- Anyone who charges GST has to mention the GST registration number on the bill.

- GST is applicable on every type of movement of goods/services.

- The rates of GST are 0%, 5%, 12%, 18% and 28% as applicable.

Common Mistakes

Percentage calculation error:

One needs to be very proficient in calculating percentages of numbers, as GST calculation revolves around finding percentages.

Watch our video on Percentages: click here

Practice Example:

Rohit purchased an article and paid GST of Rs. 10,400. He sold the article to Manish and collected GST of Rs. 11,000. Geeta purchased the same article from Manish and paid GST of Rs. 11,800. Find the amount of SGST and CGST payable at each stage if each transaction is intra state.

Solution: Click here

Calculation of GST without considering the discount

GST has to be calculated on discounted price not on the marked price.

Practice Example:

A wholesaler dealing in electric goods, sells an article at its printed price of Rs. 45,000 to a dealer at 10% discount. The dealer sells the same article to a customer at a discount of 4% on its printed price. If the sales are inter-state and the rate of GST is 18%, find:

-

the amount of tax, under GST, paid by the dealer to the central and state governments.

-

the amount of tax, under GST, received by central and state governments.

-

the total amount, inclusive of tax, paid by the consumer for the article.

Solution: Click here

Differentiating between Inter and Intra

If the transaction of goods or services happen within the same state, then it is Intra-state transaction.

If the transaction of goods or services happen from one state to another state, then it is Inter-state transaction.

Practice Example:

Find the amount of bill for the following intra-state transaction of goods/services. The GST rate is 5%

|

Quantity (No. of Items) |

MRP of each item (in Rs.) |

Discount % |

|

36 |

450 |

10 |

|

48 |

720 |

20 |

|

60 |

300 |

30 |

|

24 |

360 |

20 |

Solution: Click here

Computing SGST and CGST but not calculating the total GST

When we calculate CGST and SGST, in the case of Intra-State transactions, it is also required that we calculate the Total GST.

Total GST = SGST + CGST

Practice Example:

A shopkeeper sells an A.C. to Ms. Alka for Rs. 31,200 including GST at the rate of 28%. If the shopkeeper and Ms. Alka both are from the same city, find for the shopkeeper:

-

total amount of GST

-

taxable value of A.C.

-

amount of CGST

-

amount of SGST

Solution: Click here

TopperLearning GST Resources

Conclusion

In short, to ace GST one must be proficient in solving examples of percentage and should practice more examples involving interstate and intrastate transactions.

At TopperLearning, we bring you unique e-learning experiences, providing quality resources to students all over the country. The study materials are available for CBSE, ICSE, and Maharashtra Board alongside the resources for competitive exams like JEE and NEET.

|

1st : x > y Eg: 4 < 5 |

2nd : x ≥ y Eg: y ≥ 6 |

|

3rd : x < y Eg: x – 4 < y + 9 |

4th : x ≤ y Eg: x + 5 ≤ 10 |

More from Education

Important Resources

- Education Franchisee opportunity

- NCERT Solution

- CBSE Class 9 Mathematics

- NCERT Solutions for class 10 Science

- Sample Papers

- CBSE Class 9 Science

- NCERT Solutions for class 10 Maths

- Revision Notes

- CBSE Class 10 Hindi

- CBSE Class 10 English

- CBSE Class 10 English

- CBSE Class 10 Social Studies

- CBSE Class 10 Science

- CBSE Class 10 Mathematics

- Career In Science After 10

- Career In Commerce After 10

- Career In Humanities/Arts After 10

- NCERT Solutions for Class 10

- NCERT Solutions for Class 11

- Business Studies Class 12 CBSE project