Class 12-commerce NCERT Solutions Accountancy Chapter 2 - Reconstitution of a Partnership Firm - Admission of a Partner

The NCERT solutions for CBSE Class 12 Commerce Accountancy Chapter Reconstitution of a Partnership Firm - Admission of a Partner at TopperLearning help students learn the chapter better. The detailed solutions answer questions on every page and every exercise. These textbook solutions are helpful not only to write answers but for overall learning as well. Along with the NCERT solutions, students can also refer to our sample papers, past years’ papers, revision notes, video lessons etc.

Reconstitution of a Partnership Firm - Admission of a Partner Exercise 158

Solution SA 1

Various matters which need to be adjusted at the time of admission of a new partner are as follows:

- Profit-sharing Ratio: Determining new profit-sharing ratio

- Goodwill: Valuation and treatment of goodwill

- Revaluation of Assets and Liabilities: Profits or losses arising from revaluation of assets and liabilities are to be adjusted among old partners in the old ratio

- Accumulated Profits, Losses and Reserves: Accumulated profits, losses and reserves are distributed among old partners in the old ratio

- Capital Adjustment: Adjustment of partner's capital (if agreed)

Solution SA 2

It is necessary to ascertain new profit-sharing ratio for old partners when new partner/s is/are admitted because the old partner of the partnership firm needs to sacrifice the share of profit in favour of the new partner/s and this reduces the share of profit of old partners.

Solution SA 3

The ratio in which the existing partners of the partnership firm agree to sacrifice their share of profit in favour of the new incoming partner is called sacrificing ratio. Sacrificing ratio is calculated as the difference between old ratio and new ratio of old partners.

Sacrificing Ratio = Old Ratio - New Ratio

It is important to calculate this ratio because the new partner needs to compensate the old partners for sacrificing their share of profit. The new partner compensates the old partner by making payment to them in the form of goodwill which is transferred among the old partners in their sacrificing ratio.

Solution SA 4

Sacrificing ratio is used on the following occasions:

- When the existing partners of the partnership firm mutually decide to change the profit-sharing ratio among them.

- When a new partner is admitted in the partnership firm and the amount brought by him/her as goodwill is transferred between the old partners in their sacrificing ratio.

Solution SA 5

If goodwill already exists in the books of the old firm before the new partner/s bring in his/her share of goodwill in cash, then the existing goodwill should be written off between the old partners in their old profit-sharing ratio. Journal entry passed for the following:

|

Old Partner's Capital A/c |

Dr. |

|

------To Goodwill A/c |

|

|

(Being goodwill written off in the old ratio between old partners) |

|

Solution SA 6

When a new partner is admitted in the firm, it becomes essential to revalue assets and liabilities of the partnership firm for determining its true and fair value. Revaluation is done because the value of assets and liabilities may have increased or decreased and thus their corresponding figures in the old balance sheet may be either understated or overstated. Also, it may be possible that some of the assets and liabilities are left to be recorded. Hence, to record the increase and decrease in the market value of the assets and liabilities, the revaluation account is prepared and any profits (or losses) linked with this increase or decrease will be distributed between the old partners of the firm in their old profit-sharing ratio.

Reconstitution of a Partnership Firm - Admission of a Partner Exercise 159

Solution LA 1

Revaluation means valuation of assets and liabilities at the time of reconstitution of the firm. The reasons for the revaluation of assets and liabilities at the time of admission of a partner are

- The book values of assets and liabilities may have changed over a period of time since the firm was doing its operations.

- The admitted partner may be of the opinion that the firm has exaggerated the value of assets or shown the liabilities at a lower value.

- Old partners may think that the value of assets has increased over a period of time and are being shown at a lower value.

Accounting Entries in the Books of Accounts:

The following journal entries are recorded in the Revaluation Account on the date of admission of a new partner:

|

i. For increase in value of assets: |

|

|

Assets A/c |

Dr. |

|

------To Revaluation A/c |

|

|

(Being increase in the value of assets) |

|

|

|

|

|

ii. For decrease in value of assets: |

|

|

Revaluation A/c |

Dr. |

|

------To Asset A/c |

|

|

(Being decrease in the value of assets) |

|

|

|

|

|

iii. For increase in liabilities: |

|

|

Revaluation A/c |

Dr. |

|

------To Liabilities A/c |

|

|

(Being increase in the value of liabilities) |

|

|

|

|

|

iv. For decrease in liabilities: |

|

|

Liabilities A/c |

Dr. |

|

------To Revaluation A/c |

|

|

(Being decrease in the value of liabilities) |

|

|

|

|

|

v. For recording of unrecorded assets: |

|

|

Unrecorded Assets A/c |

Dr. |

|

------To Revaluation A/c |

|

|

(Being recording of unrecorded assets) |

|

|

|

|

|

vi. For recording of unrecorded liabilities: |

|

|

Revaluation A/c |

Dr. |

|

------To Unrecorded Liabilities A/c |

|

|

(Being recording of unrecorded liabilities) |

|

|

|

|

|

vii. For transfer of credit balance of Revaluation Account |

|

|

Revaluation A/c |

Dr. |

|

------To Old Partner's Capital A/c |

|

|

(Being profit on revaluation transferred to the Old Partner's Capital Account in their old profit-sharing ratio) |

|

|

|

|

|

OR

|

|

|

vii. For transfer of debit balance of Revaluation Account: |

|

|

Old Partner's Capital A/c |

Dr |

|

------To Revaluation A/c |

|

|

(Being loss on revaluation transferred to the Old Partner's Capital Account in their old profit-sharing ratio) |

|

Solution LA 2

Goodwill is an intangible asset which represents the value of a firm's reputation and its good brand name in the market. A firm earns goodwill by its hardwork and thereby wins the blind trust and faith of customers by fulfilling their demands in both qualitative and quantitative aspects. Positive goodwill helps a firm to earn supernormal profits compared to its competitors which earn normal profits (as their goodwill is zero). In other words, goodwill ensures greater future profits as there will be greater number of satisfied customers in the future. Goodwill is nothing more than the probability that the old customer is retained.

Characteristics of Goodwill

The following are the characteristics of goodwill:

- Is an intangible asset

- Is not a fictitious asset

- Ascertaining the exact value of goodwill is difficult

- Enhances the future and present earning capacity of a business

- Helps a firm earn supernormal profits

- Assists the business to enjoy its upper hand over its competitors

Factors Affecting Goodwill

Important factors which affect the goodwill of a firm:

- Quality of Products: A company producing best quality or superior quality products in large scale earns more goodwill.

- Location: If a business is located at easy to reach and convenient place, it provides an access to more number of consumers who will be attracted again and will lead to increase in sales over a period of time. Therefore, in some time, the firm will earn higher goodwill.

- Efficient Management: Efficient management leads to cost efficiency and increases productivity. Efficient management means superior quality products at lower cost or which can be sold at lesser price. Superior quality at lower price enables a firm to earn higher goodwill.

- Market Structure: If a firm is operating in a monopoly market with no close substitutes, then there will be more goodwill of the firm.

- Special Advantages: A firm enjoying privileges such as continuous supply of power, fuel and raw materials at a low price enjoys higher value of goodwill.

Solution LA 3

Four methods of valuation of goodwill:

1. Average Profit Method: Goodwill is calculated on the average basis of the profits of past few years. The formula for calculating goodwill is

Number of Years Purchase implies number of years for which the firm expects to earn the same amount of profits. Steps to calculate goodwill by the average profit method:

Step 1: Ascertain the total profit of past given years

Step 2: Add Abnormal losses like loss by fire and theft

Step 3: Add All normal incomes if not added previously

Step 4: Less All non-business incomes and all abnormal gains and incomes like speculation and lottery

Step 5: Less All normal expenses if not deducted previously

Step 6: Calculate Average Profit, by dividing the total profit ascertained in Step 5 by number of years

Step 7: Multiply the Average Profit to the Number of Years' Purchases to calculate the Value of Goodwill

Example:

The profits for last 5 years are Rs 2,00,000, 6,00,000, (4,00,000), 10,00,000, 16,00,000. Calculate goodwill on the basis of 4 years purchase.

2. Weight Average Method: Weights are assigned for each year's profit in a manner where higher weights are assigned to the recent year's profit and lower weights are assigned to the past year's profits. The products of the profits and the weights are added and divided by the total weights to calculate Weighted Average Profits. The formula for calculating goodwill by this method is

![]()

Steps to Calculate Goodwill by Weight Average Method:

Step 1: Assign weights to ever year. More recent years with higher weight

Step 2: Multiply the weights with its corresponding year's profits

Step 3: Calculate the total of the products

Step 4: Divide the total of the product by the total of the weights to calculate Weighted Average Profit

Step 5: Multiply the Weighted Average Profit by the number of years purchase

Example:

The profits for the last 5 years are Rs 2,00,000, Rs 6,00,000, Rs (4,00,000), Rs 10,00,000, Rs 16,00,000

Calculate goodwill on the basis of 4 years purchase.

|

Profit/Loss

|

Weights |

Product

|

|

2,00,000 |

1 |

2,00,000 × 1 = 2,00,000 |

|

6,00,000 |

2 |

6,00,000 × 2 = 12,00,000 |

|

(4,00,000) |

3 |

(4,00,000) × 3 = (12,00,000) |

|

10,00,000 |

4 |

10,00,000 × 4 = 40,00,000 |

|

16,00,000 |

5 |

16,00,000 × 5 = 80,00,000 |

|

Total |

15 |

1,22,00,000 |

3. Super Profit Method: Here, goodwill is calculated on the basis of excess profit earned by a firm over and above the normal profit earned by its counterparts in the same industry. The excess profit over the normal profit is termed Super Normal Profit.

Steps to Calculate Goodwill by Super Profit Method:

Step 1: Calculate Average Profit

Step 2: Calculate Average Capital Employed as

Step 3: Calculated Normal Profit by the formula:

![]()

Step 4: Calculate Super Normal Profit by the formula:

Super Normal Profit = Average Profit - Normal Profit

Step 5: Multiply the Super Normal Profit by the Number of Years Purchase to calculate goodwill.

4. Capitalisation Method: There are two methods of capitalisation:

a. By capitalisation of Average Profit

b. By capitalisation of Super Profit

a. Capitalisation of Average Profit

Step 1: Calculate Average Profit

Step 2: Calculate Capitalised Value of Average Profit by the following formula:

![]()

Step 3: Ascertain Actual Capital EmployedStep 4: Deduct Actual Capital Employed from Capitalised Average Profit to calculate goodwill.

Goodwill = Capitalised Average Profit - Actual Capital Employed

b. Capitalisation of Super Profit

Step 1: Calculate the Capital Employed

Step 2: Calculate Normal Profit by the following formula:

![]()

Step 3: Calculate Average Profit

Step 4: Calculate Super Normal Profit by the following formula:

Super Normal Profit = Average Profit - Normal Profit

Step 5: Calculate goodwill by the following formula:

![]()

Solution LA 4

In case a new partner is admitted to the firm, it may be agreed that the capital of all partners should be proportionate to the new profit-sharing ratio. In such cases, the working of new capital of each partner is based on two of the following cases:

- Capital of the new partner is given

- Total capital of the firm is given

1. When the capital of the new partner is given

In this situation, the calculation of the new capital of all partners involves the following steps:

Step 1: Calculate the total capital of the new firm on the basis of capital of the new partner

Step 2: Divide the total capital of the firm by the individual share of profits of partners to ascertain new capital of each partner

Step 3: Ascertain partner's capital balance (credit-debit) after posting all adjustments

Step 4: The new balance as ascertained in Step 2 is written on the credit side of the Partner's Capital Account.

Step 5: Calculate Surplus or Deficit. If the new capital (Step 2) exceeds the old capital (Step 3), then it is termed 'Deficit' and the difference amount is to be brought in by the old partners. If the new capital is lesser than old capital, then it is termed 'Surplus' and the difference amount is returned to the old partners.

Example:

L and M are partners sharing profit and loss equally. They agree to admit N for ![]() share in profit. N brings Rs 25,000 as capital. The old capitals of L and M are Rs 30,000 and Rs 20,000, respectively, at the time admission of N.

share in profit. N brings Rs 25,000 as capital. The old capitals of L and M are Rs 30,000 and Rs 20,000, respectively, at the time admission of N.

Step 1: The total capital of the new firm on the basis of N's Capital![]()

Step 2:

![]()

![]()

Step 3:

|

|

L |

M |

|

New Capital |

25,000 |

25,000 |

|

Less: Existing Capital |

(30,000) |

(20,000) |

|

Surplus (Deficit) |

5,000 |

(5,000) |

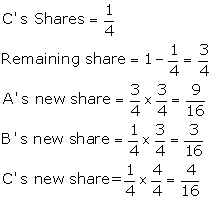

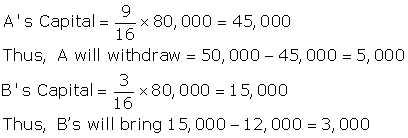

2. When the total capital of the new firm is given: When the capital of the new partner is not mentioned, his/her capital is ascertained on the proportionate basis of total capital of the firm. The capital ascertained is to be brought in by the new partner in form of his/her portion of capital. To ascertain the proportionate capital of the new partner, the following steps are to be followed:

Step 1: Ascertain the total old capital of the old partners after making all adjustments

Step 2: Multiply the total of old partner's capital (Step 1) with reciprocal of total share of old partners to ascertain the total capital of the new firm

Total Capital of New Firm = Total Capital of the Old Partners × Reciprocal of the Combined New Share of the Old Partners

Step 3: Calculate new capital of each partner on the basis of total capital. This is done by multiplying the Total Capital by the new profit-sharing ratio individually for all partners including the new partner.

Example:

A and B are partners in a firm sharing profit and loss equally. They agree to admit C for ![]() share in profit and decided to share future profit and loss equally. A's capital is 4,00,000 and B's capital is 3,00,000. C brings sufficient capital for his share in profit.

share in profit and decided to share future profit and loss equally. A's capital is 4,00,000 and B's capital is 3,00,000. C brings sufficient capital for his share in profit.

Step 1: Calculation of Total Capital of Old Partners (after all adjustments)

The total capital of the old partners = Rs. 4,00,000 + Rs. 3,00,000 = Rs. 7,00,000

Step 2: Calculation of Total Capital of New Firm

Total Capital of New Firm = Total Capital of the Old Partners × Reciprocal of the Combined New Share of the Old Partners

![]()

Step 3: Calculation of New Capital of Each Partner

Solution LA 5

When a new partner enters a partnership firm, the old partner sacrifices his share for him, so it is the duty of the new partner to give goodwill in cash or in any other way to the old partner. In case the new partner is not in a position to bring his share of goodwill in cash, then a goodwill account is adjusted through the old Partner's Capital Account. The New Partner's Capital Account or Current Account is debited with his/her share of goodwill and partners who sacrifice their share in favour of the new partner are credited in their sacrificing ratio.

Also, according to Para 16 of Accounting, Standard 10, goodwill is recorded in the books only when some consideration in money or money's worth has been paid for it. It is mandatory to follow this practice. For admission, retirement. death or change in profit-sharing ratio among existing partners, a Goodwill Account cannot be raised as no consideration is paid for it.

The following are journal entries recorded in the books of accounts if a new partner is not able to bring goodwill in cash.

|

New Partner's Capital A/c |

Dr. |

|

------To Old Partners' Capital A/c |

|

|

(Being new partner capital account is debited with his/her share of goodwill and sacrificing Partner's Capital Account are credited in their sacrificing ratio) |

|

|

|

|

Solution LA 6

Two methods for the treatment of goodwill at the admission of a new partner include

- Premium Method

- Revaluation Method

Any of the two methods can be adopted, but before that it is necessary that if any goodwill already appears in the old books of the firm, then first, that should be written off among all the old partners in their old profit-sharing ratio. The following journal entry is passed to distribute the goodwill:

|

Old Partners' Capital A/c |

Dr. |

|

------To Goodwill A/c |

|

|

(Being goodwill written off among the old partners in their old profit-sharing ratio) |

|

|

|

|

Treatment of Goodwill

1. Premium Method: It is used when the new partner pays his or her share of goodwill in cash. The accounting treatment under this depends on the situation and scenarios which include

i. If the new partner privately pays his/her share of goodwill to the old partners: No accounting treatment is required to be done as the goodwill is privately paid.

ii. When the new partner brings his/her share of goodwill in cash and the goodwill is retained in the business.

Accounting Entries

|

a. For premium or goodwill brought in cash by the new partner |

|

|

Cash/Bank A/c |

Dr. |

|

------To Premium for Goodwill A/c |

|

|

(Being amount of goodwill brought in by the new partner) |

|

|

|

|

|

b. For transferring of new partner's goodwill among the old partners, i.e. if goodwill is retained in the business. |

|

|

Premium for Goodwill A/c |

Dr. |

|

------To Sacrificing Partner's Capital A/c |

|

|

(Being goodwill brought in by the new partner distributed among the old partners in their sacrificing ratio) |

|

|

|

|

|

c. If the new partner's share of goodwill is withdrawn by the old partner, then |

|

|

Sacrificing Partner's Capital A/c |

Dr. |

|

------To Cash A/c |

|

|

(Being amount of goodwill withdrawn by the old partners) |

|

|

|

|

iii. If the new partner partly brings his/her share of goodwill

|

a. For bringing goodwill in cash |

|

|

|

Cash A/c |

Dr. |

|

|

------To Premium for Goodwill A/c |

|

|

|

(Being amount of goodwill brought in cash by the new partner) |

|

|

|

|

|

|

|

b. For transferring goodwill to the old partners |

|

|

|

Goodwill A/c |

Dr. |

(With the amount of goodwill brought in by the new partner) |

|

New Partner's Capital A/c |

Dr. |

(With the amount of goodwill not brought in by the partner) |

|

------To Sacrificing Partner's Capital A/c |

|

|

|

(Being goodwill amount of the new partner distributed among the old partners in their sacrificing ratio) |

|

|

|

|

|

|

2. Revaluation Method: This method is adopted when the new partner is not able to bring goodwill in cash at all.

|

New Partner's Capital A/c |

Dr. |

(With the whole amount of goodwill that is not brought in by the new partner) |

|

------To Old Partner's Capital A/c |

|

|

|

(Being amount of goodwill brought in cash by the new partner) |

|

|

|

|

|

|

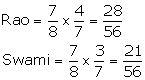

Solution LA 7

The profits or losses which have accumulated over the years and have not been credited or debited to the partners capital account are called accumulated or undistributed profits or losses. In case a new partner is admitted to the partnership firm, then all the past accumulated profits or losses and the reserves are to be distributed among all the old partners in their old profit-sharing ratio. This is because these profits and losses are attributable to the hardwork and labours of the old partners, and consequently, the old partners are liable to bear losses, if any. The new partner is not entitled to a share in these profits/losses as he/she was not part of such efforts or hard earned profits/losses and accordingly is not responsible for the past performance of the business.

Accounting Treatment of Accumulated Profits and Losses

|

i. Distributing Accumulated Profits and Reserves |

|

|

Profit and Loss A/c |

Dr. |

|

General Reserve A/c |

Dr. |

|

Reserve Fund A/c |

Dr. |

|

Workmen's Compensation Fund A/c |

Dr. |

|

Contingency Reserve A/c |

Dr. |

|

------To Old Partner's Capital A/c |

|

|

(Being undistributed profits and reserves distributed among old partners in their old profit-sharing ratio) |

|

|

|

|

|

ii. Distributing Accumulated Losses |

|

|

Old Partners' Capital A/c |

Dr. |

|

------To Profit and Loss (Debit balance) A/c |

|

|

------To Deferred Advertisement Expenses A/c |

|

|

------To Preliminary Expenses A/c |

|

|

(Being undistributed losses distributed among old partners in their old profit-sharing ratio) |

|

|

|

|

Solution LA 8

After revaluation of assets and liabilities has been done for the newly constituted partnership firm, all the assets and liabilities appear at their current market values including any unrecorded asset or liability in the Balance Sheet. This is evident from the example given below:

X, Y and Z were partners in a firm sharing profits in the ratio of 3:2:1, respectively. The Balance Sheet of the firm on 31st March 2015 stood as follows:

|

Liabilities |

Rs. |

Assets |

|

Rs. |

|

Sundry Creditors |

9,500 |

Bank Balance |

|

1,250 |

|

Bills Payable |

2,500 |

Debtors |

8,000 |

|

|

General Reserve |

6,000 |

Less: Provision |

250 |

7,750 |

|

X's Capital A/c |

20,000 |

Stock |

|

12,500 |

|

Y's Capital A/c |

15,000 |

Motor Van |

|

4,000 |

|

Z's Capital A/c |

12,500 |

Machinery |

|

17,500 |

|

|

|

Buildings |

|

22,500 |

|

|

65,500 |

|

|

65,500 |

Y retired from the firm on the above date subject to the following conditions:

Goodwill of the firm be valued at Rs 9,000. Machinery would be depreciated by 10% and Motor Van by 15%. Stock would be appreciated by 20% and Building by 10%. The provision for doubtful debts would be increased by Rs 975. Liability for workmen compensation to the extent of Rs 825 would be created.

It was agreed that X and Z would share profits in the future in the ratio of 3:2, respectively.

Revaluation Account, Capital Account and Balance Sheet of the new firm:

|

Revaluation Account |

|||

|

Particulars |

Rs. |

Particulars |

Rs. |

|

To Machinery |

1,750 |

By Stock |

2,500 |

|

To Provision for doubtful debt |

975 |

By Building |

2,250 |

|

To Motor Van |

600 |

|

|

|

To Workmen Claim |

825 |

|

|

|

To Profit Transferred: |

|

|

|

|

X |

300 |

|

|

|

Y |

200 |

|

|

|

Z |

100 |

|

|

|

|

4,750 |

|

4,750 |

|

Capital Account |

|||||||

|

Particulars |

X |

Y |

Z |

Particulars |

X |

Y |

Z |

|

To Y's Cap. |

900 |

|

2,100 |

By Bal. b/d |

20,000 |

15,000 |

12,500 |

|

To Y's Loan |

|

20,200 |

|

By Rev. A/c |

300 |

200 |

100 |

|

To Bal. c/d |

22,400 |

|

11,500 |

By Gen. Res. |

3,000 |

2,000 |

1,000 |

|

|

|

|

|

By X's Cap. |

|

900 |

|

|

|

|

|

|

By Z's Cap. |

|

2,100 |

|

|

|

|

|

|

|

|

|

|

|

|

23,300 |

20,200 |

13,600 |

|

23,300 |

20,200 |

13,600 |

|

Balance Sheet |

||||

|

Liabilities |

Rs. |

Assets |

|

Rs. |

|

Sundry Creditors |

9,500 |

Bank Balance |

|

1,250 |

|

Bills Payable |

2,500 |

Debtors |

8,000 |

|

|

Workmen Claim |

825 |

Less: Provision |

1,225 |

6,775 |

|

X's Capital A/c |

22,400 |

Stock |

|

15,000 |

|

Z's Capital A/c |

11,500 |

Motor Vans |

|

3,400 |

|

Y's Loan |

20,200 |

Machinery |

|

15,750 |

|

|

|

Buildings |

|

24,750 |

|

|

66,925 |

|

|

66,925 |

Note: Gain Ratio = 3:7

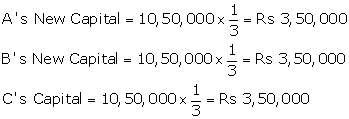

Solution NUM 1

|

|

A :B |

|

Old Ratio= |

3 :2 |

|

|

OR |

|

= |

|

![]()

Let new firm profit = 1

Remaining share of A and B in the new firm

= 1- C's share

New Ratio = Old Ratio × Remaining Share

|

|

A: |

B |

:C |

|

New Ratio= |

|

|

|

|

|

|

||

Solution NUM 2

|

|

A: |

B |

:C |

|

Old Ratio= |

3: |

2: |

1 |

|

= |

|

|

|

![]()

Let new firm profit = 1

Remaining share of A, B and C in new firm

= 1 - D's share

New Ratio = Old Ratio × Remaining Share

|

|

A: |

B |

:C |

:D |

|

New Ratio= |

|

|

|

|

Solution NUM 3

|

|

A: |

B |

|

Old Ratio = |

5: |

3 |

|

= |

|

|

![]()

![]()

New Ratio = Old Ratio - Sacrificing Ratio

|

|

A: |

B |

:C |

|

New Ratio= |

|

|

|

Solution NUM 4

|

|

A: |

B |

:C |

|

Old Ratio= |

2: |

2: |

1 |

|

= |

|

|

|

D admits for ![]() share in the new firm, which he taken from A.

share in the new firm, which he taken from A.

Here only A will sacrifice.

New Ratio = Old Ratio - Sacrificing Ratio

![]()

|

|

A: |

B |

:C |

:D |

|

New Ratio= |

|

|

|

|

Solution NUM 5

|

|

P: |

Q |

|

Old Ratio = |

2: |

1 |

|

= |

|

|

New Ratio = Old Ratio - Sacrificing Ratio

|

|

P: |

Q |

:R |

|

New Ratio= |

|

|

|

Solution NUM 6

|

|

A: |

B |

:C |

|

Old Ratio= |

3: |

2: |

2 |

|

= |

|

|

|

New Ratio = Old Ratio - Sacrificing Ratio

|

|

A: |

B |

:C |

:D |

|

New Ratio= |

|

|

|

|

Reconstitution of a Partnership Firm - Admission of a Partner Exercise 160

Solution NUM 7

|

|

A: |

B |

|

Old Ratio = |

3: |

2 |

|

= |

|

|

![]()

New Ratio = Old Ratio - Sacrificing Ratio

|

|

A: |

B |

:C |

|

New Ratio= |

|

|

|

Solution NUM 8

|

|

A: |

B |

:C |

|

Old Ratio = |

3: |

3: |

2 |

|

= |

|

|

|

![]()

|

D's share = |

A's Sacrifice + |

B's Sacrifice + |

C's Sacrifice |

|

|

|

|

|

New Ratio = Old Ratio - Sacrificing Ratio

|

|

A: |

B |

:C |

:D |

|

New Ratio= |

|

|

|

|

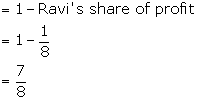

Solution NUM 9

|

|

Radha: |

Rukmani |

|

Old Ratio = |

3: |

2 |

|

= |

|

|

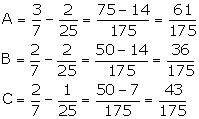

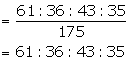

![]()

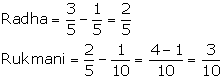

![]()

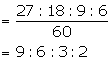

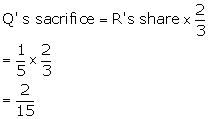

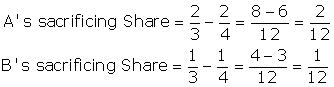

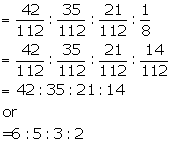

Sacrificing Ratio = Old Ratio × Surrender Ratio

New Ratio = Old Ratio - Sacrificing Ratio

Gopi's Share = Radha's Sacrificing Ratio + Rukmani's Sacrificing Ratio

|

|

Radha: |

Rukmani: |

:Gopi |

|

New Ratio= |

|

|

|

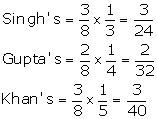

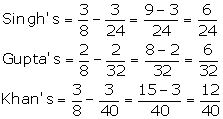

Solution NUM 10

|

|

Singh: |

Gupta |

:Khan |

|

Old Ratio = |

3: |

2: |

3 |

|

= |

|

|

|

![]()

![]()

![]()

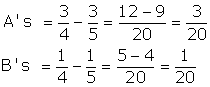

Sacrificing Ratio = Old Ratio × Surrender Ratio

|

|

Singh's Sacrifice + |

Gupta's Sacrifice + |

Khan's Sacrifice |

|

Jain's Share= |

|

|

|

New Ratio = Old Ratio - Sacrificing Ratio

|

|

Singh: |

Gupta: |

Khan: |

Jain |

|

New Ratio= |

|

|

|

|

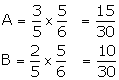

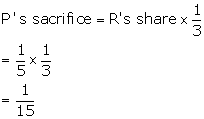

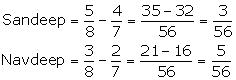

Solution NUM 11

|

|

Sandeep: |

Navdeep |

|

Old Ratio = |

5: |

3 |

|

= |

|

|

|

|

Sandeep: |

Nevdeep: |

C |

|

New Ratio= |

4: |

2: |

1 |

|

= |

|

|

|

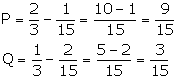

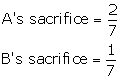

Sacrificing Ratio = Old Ratio -New Ratio

|

|

Sandeep: |

Navdeep |

|

Sacrifice Ratio= |

|

|

|

|

3: |

5 |

Note: Answer given the book is different. However, as per the solution sacrificing ratio is 3:5.

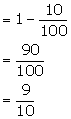

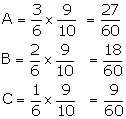

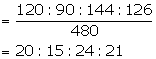

Solution NUM 12

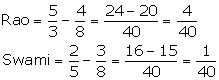

|

|

Rao: |

Swami |

|

Old Ratio= |

3: |

2 |

![]()

Let the New Firm Profit =1

Combined share of Rao and Swami in the new firm

New Ratio = Combined Share of Rao and Swami × Proportion of Rao and Swami in the Combined Share

|

|

Rao: |

Swami: |

C |

|

New Ratio = |

|

|

|

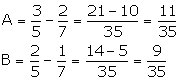

Sacrificing Ratio = Old Ratio -New Ratio

|

Sacrifice Ratio= |

Rao: |

Swami |

|

|

= |

|

|

|

|

= |

4: |

1 |

|

Solution NUM 13

![]()

|

Year |

Profit |

|

2013 |

40,000 |

|

2014 |

50,000 |

|

2015 |

60,000 |

|

2016 |

50,000 |

|

2017 |

60,000 |

|

Sum of 5 years profit |

2,60,000 |

= Rs.2,08,000

Solution NUM 14

Capital Employed = Rs.2,00,000

Actual Profit = 48,000

Normal Rate of Return = 15%

= Rs.30,000

Super profit = Actual Profit - Normal Profit

=48,000 - 30,000

= Rs.18,000

Goodwill = Super Profit × Number of Years Purchase

=18,000 × 3

= Rs.54,000

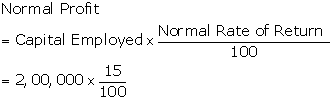

Solution NUM 15

![]()

|

Year |

Profit |

|

2015 |

40,000 |

|

2014 |

50,000 |

|

2013 |

55,000 |

|

2012 |

70,000 |

|

2011 |

85,000 |

|

Sum of 5 years profit |

3,00,000 |

Average Super profit = Actual Profit - Normal Profit

=60,000 - 50,000

= Rs.10,000

Goodwill = Super Profit × Number of Years Purchase

=10,000 × 3

= Rs.30,000

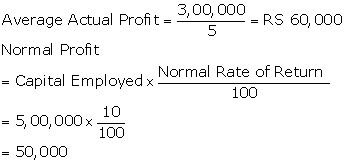

Reconstitution of a Partnership Firm - Admission of a Partner Exercise 161

Solution NUM 16

|

Rajan's Capital |

3,00,000 |

|

Rajni's Capital |

2,00,000 |

|

Total Capital Employed |

5,00,000 |

Normal Rate of Return =20%

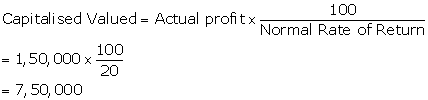

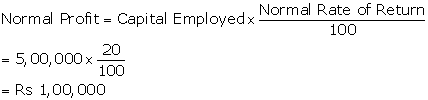

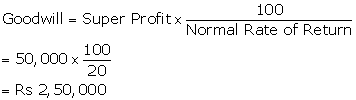

Goodwill = Capitalised Value - Capital Employed

=7,50,000 - 5,00,000

= Rs.2,50,000

Alternative Method

Super profit = Actual Profit - Normal Profit

=1,50,000 - 1,00,000

=Rs 50,000

Solution NUM 17

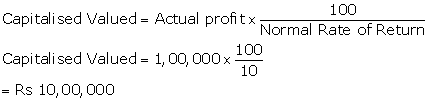

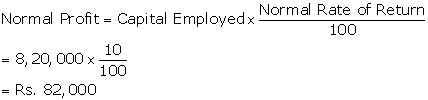

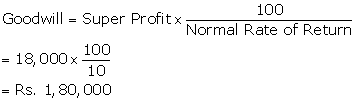

Goodwill = Capitalised Value - Capital Employed

=10,00,000 - 8,20,000

= Rs.1,80,000

Alternative Method

Capital Employed = Assets - External Liabilities

= 10,00,000 - 1,80,000

= Rs.8,20,000

Super profit = Actual Profit - Normal Profit

=1,00,000 - 82,000

= Rs.18,000

Solution NUM 18

|

Journal Entries |

|||||

|

Sr. No. |

Particulars |

|

L.F. |

Dr. Rs. |

Cr. Rs. |

|

Case a. |

Cash A/c |

Dr. |

|

24,000 |

|

|

|

------To Ghosh's Capital A/c |

|

|

|

20,000 |

|

|

------To Premium for Goodwill A/c |

|

|

|

4,000 |

|

|

(Being capital and goodwill brought by Ghosh) |

|

|

|

|

|

|

|

|

|

|

|

|

|

Premium for Goodwill A/c |

Dr. |

|

4,000 |

|

|

|

------To Verma's Capital A/c |

|

|

|

2,500 |

|

|

------To Sharma's Capital A/c |

|

|

|

1,500 |

|

|

(Being goodwill brought by Ghosh credited to old partners in Sacrificing ratio) |

|

|

|

|

|

|

|

|

|

|

|

|

Case b. |

Cash A/c |

Dr. |

|

24,000 |

|

|

|

------To Ghosh's Capital A/c |

|

|

|

20,000 |

|

|

------To Premium for Goodwill A/c |

|

|

|

4,000 |

|

|

(Being capital and Goodwill brought by Ghosh for his (1/5) share of profit ) |

|

|

|

|

|

|

|

|

|

|

|

|

|

Premium for Goodwill A/c |

Dr. |

|

4,000 |

|

|

|

------To Verma's Capital A/c |

|

|

|

2,500 |

|

|

------To Sharma's Capital A/c |

|

|

|

1,500 |

|

|

(Being goodwill brought by Ghosh credited in old partners in Sacrificing ratio) |

|

|

|

|

|

|

|

|

|

|

|

|

|

Verma's Capital A/c |

Dr. |

|

2,500 |

|

|

|

Sharma's Capital A/c |

Dr. |

|

1,500 |

|

|

|

------To Cash A/c |

|

|

|

4,000 |

|

|

(Being amount of premium for Goodwill withdrawn by Old Partners) |

|

|

|

|

|

|

|

|

|

|

|

|

Case c. |

Cash A/c |

Dr. |

|

24,000 |

|

|

|

------To Ghosh's Capital A/c |

|

|

|

20,000 |

|

|

------To Premium for Goodwill A/c |

|

|

|

4,000 |

|

|

(Being capital and Goodwill brought by Ghosh for his (1/5) share of profit ) |

|

|

|

|

|

|

|

|

|

|

|

|

|

Premium for Goodwill A/c |

Dr. |

|

4,000 |

|

|

|

------To Verma's Capital A/c |

|

|

|

2,500 |

|

|

------To Sharma's Capital A/c |

|

|

|

1,500 |

|

|

(Being premium for goodwill credited to old partner's Capital Account in sacrificing ratio) |

|

|

|

|

|

|

|

|

|

|

|

|

|

Verma's Capital A/c |

Dr. |

|

1,250 |

|

|

|

Sharma's Capital A/c |

Dr. |

|

750 |

|

|

|

------To Cash A/c |

|

|

|

2,000 |

|

|

(Being 50% of the amount of premium for goodwill withdrawn by old partners) |

|

|

|

|

|

|

|

|

|

|

|

|

Case d. |

No entry because Goodwill was not brought in to firm |

|

|

|

|

|

|

|

|

|

|

|

Solution NUM 19

|

Journal Entries |

|||||

|

Date |

Particulars |

|

L.F. |

Dr. Rs. |

Cr. Rs. |

|

|

Cash A/c |

Dr. |

|

35,000 |

|

|

|

------To C's Capital A/c |

|

|

|

30,000 |

|

|

------To Premium for Goodwill A/c |

|

|

|

5,000 |

|

|

(Being amount of capital and share of goodwill brought by C) |

|

|

|

|

|

|

|

|

|

|

|

|

|

Premium for Goodwill A/c |

Dr. |

|

5,000 |

|

|

|

------To A's Capital A/c |

|

|

|

2,000 |

|

|

------To B's Capital A/c |

|

|

|

3,000 |

|

|

(Being C's share of goodwill credited to old partners in their sacrificing ratio) |

|

|

|

|

|

|

|

|

|

|

|

|

|

A's Capital A/c |

Dr. |

|

2,000 |

|

|

|

B's Capital A/c |

Dr. |

|

3,000 |

|

|

|

------To Cash A/c |

|

|

|

5,000 |

|

|

(Being share of goodwill withdrawn by old partners) |

|

|

|

|

|

|

|

|

|

|

|

Sacrificing Ratio = Old Ratio -New Ratio

|

|

Rao: |

Swami |

|

Sacrifice Ratio= |

|

|

|

= |

2: |

3 |

Goodwill of the firm = Rs.20,000

Solution NUM 20

|

Journal Entries |

|||||

|

Date |

Particulars |

|

L.F. |

Dr. Rs. |

Cr. Rs. |

|

|

Arti's Capital A/c |

Dr. |

|

3,000 |

|

|

|

Bharti's Capital A/c |

Dr. |

|

2,000 |

|

|

|

------To Cash A/c |

|

|

|

5,000 |

|

|

(Being goodwill written off in old ratio) |

|

|

|

|

|

|

|

|

|

|

|

|

|

Cash A/c |

Dr. |

|

60,000 |

|

|

|

------To Sarthi's Capital A/c |

|

|

|

50,000 |

|

|

------To Premium for Goodwill A/c |

|

|

|

10,000 |

|

|

(Being amount of capital and share of goodwill brought by Sarthi) |

|

|

|

|

|

|

|

|

|

|

|

|

|

Premium for Goodwill A/c |

Dr. |

|

10,000 |

|

|

|

------To Arti's Capital A/c |

|

|

|

4,000 |

|

|

------To Bharti's Capital A/c |

|

|

|

6,000 |

|

|

(Being premium for goodwill credited to old partners in their sacrificing ratio) |

|

|

|

|

|

|

|

|

|

|

|

|

|

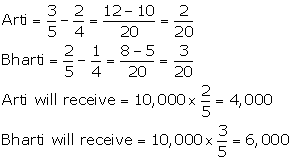

Arri: |

Bharti |

|

Old Ratio= |

3: |

2 |

![]()

|

|

Arri: |

Bharti: |

Sarthi |

|

New Ratio= |

2: |

1: |

1 |

Sacrificing Ratio = Old Ratio -New Ratio

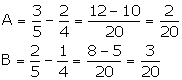

Solution NUM 21

|

Journal Entries |

|||||

|

Date |

Particulars |

|

L.F. |

Dr. Rs. |

Cr. Rs. |

|

|

Cash A/c |

Dr. |

|

27,000 |

|

|

|

------To Z's Capital A/c |

|

|

|

20,000 |

|

|

------To Premium for Goodwill A/c |

|

|

|

7,000 |

|

|

(Being amount of capital and his share of goodwill) |

|

|

|

|

|

|

|

|

|

|

|

|

|

Premium for Goodwill A/c |

Dr. |

|

7,000 |

|

|

|

------To X's Capital A/c |

|

|

|

4,000 |

|

|

------To Y's Capital A/c |

|

|

|

3,000 |

|

|

(Being premium for goodwill credit to old partners in sacrificing Ratio) r |

|

|

|

|

|

|

|

|

|

|

|

|

|

Goodwill Rs. 40,000 cannot be raised. According to AS - 10 Goodwill can be shown in the book if money and money value is paid for it. Here no money or money value has been paid for Goodwill. |

|

|

|

|

|

|

|

|

|

|

|

Note:

- According to AS - 10 Goodwill can be shown in the book if money and money value is paid for it. Here, no money or money value has been paid for Goodwill. Hence, Goodwill cannot be raised to Rs.40,000.

- Sacrificing Ratio will be equal to old ratio because new and sacrificing ratio is not given, if sacrificing and new ratio is not given it is assumed that old partners sacrificed in their old ratio.

Solution NUM 22

|

Journal Entries |

|||||

|

Date |

Particulars |

|

L.F. |

Dr. Rs. |

Cr. Rs. |

|

|

Cash A/c |

Dr. |

|

60,000 |

|

|

|

------To Christopher's Capital A/c |

|

|

|

50,000 |

|

|

------To Premium for Goodwill A/c |

|

|

|

10,000 |

|

|

(Being amount of capital and premium for goodwill brought by Christopher) |

|

|

|

|

|

|

|

|

|

|

|

|

|

Premium for Goodwill A/c |

Dr. |

|

10,000 |

|

|

|

Christopher's Capital A/c |

Dr. |

|

5,000 |

|

|

|

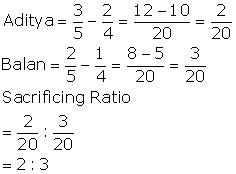

------To Aditya's Capital A/c |

|

|

|

6,000 |

|

|

------To Balan's Capital A/c |

|

|

|

9,000 |

|

|

(Being goodwill Christopher's share taken by old partner's in sacrificing ratio) |

|

|

|

|

|

|

|

|

|

|

|

Sacrificing Ratio = Old Ratio -New Ratio

Reconstitution of a Partnership Firm - Admission of a Partner Exercise 162

Solution NUM 26

|

Books of Amar, Akbar and Anthony Journal Entries |

|||||

|

Date |

Particulars |

|

L.F. |

Dr. Rs. |

Cr. Rs. |

|

|

Anthoney's Capital A/c |

Dr. |

|

45,000 |

|

|

|

------To Amar's Capital A/c |

|

|

|

11,250 |

|

|

------To Akbar's Capital A/c |

|

|

|

33,750 |

|

|

(Being adjustment of Anthony's share of goodwill) |

|

|

|

|

|

|

|

|

|

|

|

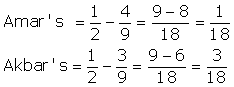

Working Notes:

1. Sacrificing Ratio = Old Ratio -New Ratio

Sacrificing Ratio between Amar and Akbar= 1:3.

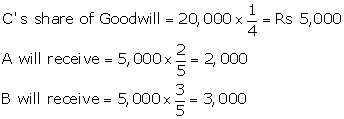

Solution NUM 23

|

|

Amar: |

Samar |

|

Old Ratio |

3: |

1 |

Kanwar admitted for 1/4 share of profit.

New Firm's Goodwill = Rs.80,000

Kanwar' s Share of Goodwill = 80,000 × 1/4 = 20,000

|

Journal Entries |

|||||

|

Date |

Particulars |

|

L.F. |

Dr. Rs. |

Cr. Rs. |

|

|

Kanwar's Capital A/c |

Dr. |

|

20,000 |

|

|

|

------To Amar's Capital A/c |

|

|

|

15,000 |

|

|

------To Samar's Capital A/c |

|

|

|

5,000 |

|

|

(Being Kanwar's share of goodwill charged from his capital account by old partners in sacrificing ratio) |

|

|

|

|

|

|

|

|

|

|

|

Note:

- Sacrificing Ratio will be equal to old ratio because new and sacrificing ratio is not given, if sacrificing and new ratio is not given it is assumed that old partners sacrificed in their old ratio.

Solution NUM 24

|

Year |

Profit |

|

2013 |

50,000 |

|

2014 |

60,000 |

|

2015 |

90,000 |

|

2016 |

70,000 |

|

Sum of 4 years profit |

2,70,000 |

Ram Lal entered into the firm for 1/4 share of Profit.

Ram Lal's share of goodwill = 2,02,500 × 1/4 =Rs.50,625

Sacrificing Ratio will be equal to old ratio because new and sacrificing ratio is not given, if sacrificing and new ratio is not given it is assumed that old partners sacrificed in their old ratio.

Mohan Lal will get = Ram Lal's Share of Goodwill × 3/5= 50,625 × 3/5= 10,125 ×3/5 =Rs.30,375

Sohan Lal will = Ram Lal's Share of Goodwill × 2/5 = 50,625 × 2/5 =10,125 × 2/5 = Rs.20,250

Case a

|

Journal Entries |

|||||

|

Date |

Particulars |

|

L.F. |

Dr. Rs. |

Cr. Rs. |

|

|

Mohan Lal's Capital A/c |

Dr. |

|

1,21,500 |

|

|

|

Sohan Lal's Capital A/c |

Dr. |

|

81,000 |

|

|

|

------To Goodwil A/c |

|

|

|

2,02,500 |

|

|

(Being goodwill appeared in the old firm written off) |

|

|

|

|

|

|

|

|

|

|

|

|

|

Ram Lal's Capital A/c |

Dr. |

|

50,625 |

|

|

|

------To Mohan Lal's Capital A/c |

|

|

|

30,375 |

|

|

------To Sohan Lal's Capital A/c |

|

|

|

20,250 |

|

|

(Being Ram Lal's share of goodwill charged from his account and distributed between old partners in sacrificing ratio) |

|

|

|

|

|

|

|

|

|

|

|

Case b

|

Journal Entries |

|||||

|

Date |

Particulars |

|

L.F. |

Dr. Rs. |

Cr. Rs. |

|

|

Mohan Lal's Capital A/c |

Dr. |

|

1,500 |

|

|

|

Sohan Lal's Capital A/c |

Dr. |

|

1,000 |

|

|

|

------To Goodwil A/c |

|

|

|

2,500 |

|

|

(Being goodwill already in the books of firm written off in ratio) |

|

|

|

|

|

|

|

|

|

|

|

|

|

Ram Lal's Capital A/c |

Dr. |

|

50,625 |

|

|

|

------To Mohan Lal's Capital A/c |

|

|

|

30,375 |

|

|

------To Sohan Lal's Capital A/c |

|

|

|

20,250 |

|

|

(Being Ram Lal's share of goodwill charged from his capital and distributed between old partners in sacrificing ratio) |

|

|

|

|

|

|

|

|

|

|

|

Case c

|

Journal Entries |

|||||

|

Date |

Particulars |

|

L.F. |

Dr. Rs. |

Cr. Rs. |

|

|

Mohan Lal's Capital A/c |

Dr. |

|

1,23,000 |

|

|

|

Sohan Lal's Capital A/c |

Dr. |

|

82,000 |

|

|

|

------To Ram Lal's Capital A/c |

|

|

|

2,05,000 |

|

|

(Being goodwill already in the books of firm written off in old ratio) |

|

|

|

|

|

|

|

|

|

|

|

|

|

Ramlal's Capital A/c |

Dr. |

|

50,625 |

|

|

|

------To Mohan Lal's Capital A/c |

|

|

|

30,375 |

|

|

------To Sohan Lal's Capital A/c |

|

|

|

20,250 |

|

|

(Being Ram Lal's share of Goodwill charged from his capital and distributed between old partners in sacrificing ratio) |

|

|

|

|

|

|

|

|

|

|

|

Solution NUM 25

|

Books of Rajesh, Mukesh and Hari Journal Entries |

|||||

|

Date |

Particulars |

|

L.F. |

Dr. Rs. |

Cr. Rs. |

|

|

Hari's Capital A/c |

Dr. |

|

8,000 |

|

|

|

------To Rajesh's Capital A/c |

|

|

|

2,000 |

|

|

------To Mukesh's Capital A/c |

|

|

|

6,000 |

|

|

(Being adjustment of Hari's share of goodwill) |

|

|

|

|

|

|

|

|

|

|

|

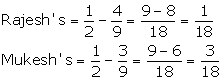

Working Notes:

1. Goodwill of a firm = Rs.36,000

Hari's share in goodwill

= Goodwill of firm × Admitting partner share

2. Sacrificing Ratio = Old Ratio -New Ratio

Sacrificing Ratio between Rajesh and Mukesh= 1:3

Solution NUM 27

|

Journal Entries |

|||||

|

Date |

Particulars |

|

L.F. |

Dr. Rs. |

Cr. Rs. |

|

2016 |

|

|

|

|

|

|

Mar 31 |

Bank A/c |

Dr. |

|

1,60,000 |

|

|

|

------To C's Capital A/c |

|

|

|

1,00,000 |

|

|

------To Premium for Goodwill A/c |

|

|

|

60,000 |

|

|

(Being capital and premium for goodwill brought by C for his 1/4th Share) |

|

|

|

|

|

|

|

|

|

|

|

|

|

Premium for Goodwill A/c |

Dr. |

|

60,000 |

|

|

|

------To A's Capital A/c |

|

|

|

40,000 |

|

|

------To B's Capital A/c |

|

|

|

20,000 |

|

|

(Being premium for goodwill brought by C transferred to old partner's in sacrificing ratio i.e., 2:1) |

|

|

|

|

|

|

|

|

|

|

|

|

|

Plant A/c |

Dr. |

|

20,000 |

|

|

|

Building A/c |

Dr. |

|

15,000 |

|

|

|

------To Revaluation A/c |

|

|

|

35,000 |

|

|

(Being increase in value of assets) |

|

|

|

|

|

|

|

|

|

|

|

|

|

Revaluation A/c |

Dr. |

|

8,000 |

|

|

|

------To Stock A/c |

|

|

|

4,000 |

|

|

------To Provision for Doubtful Debts A/c |

|

|

|

3,000 |

|

|

------To Creditors A/c (Unrecorded) |

|

|

|

1,000 |

|

|

(Being revaluation of assets and liabilities) |

|

|

|

|

|

|

|

|

|

|

|

|

|

Revaluation A/c |

Dr. |

|

27,000 |

|

|

|

------To A's Capital A/c |

|

|

|

18,000 |

|

|

------To B's Capital A/c |

|

|

|

9,000 |

|

|

(Being profit on revaluation transferred to old partners capital account) |

|

|

|

|

|

|

|

|

|

|

|

|

Revaluation Account |

||||

|

Dr. |

|

|

Cr. |

|

|

Particulars |

Amount Rs. |

Particulars |

Amount Rs. |

|

|

To Stock A/c |

|

4,000 |

By Plant A/c |

20,000 |

|

To Provision for Doubtful Debts A/c |

|

3,000 |

By Building A/c |

15,000 |

|

To Creditors (Unrecorded) A/c |

|

1,000 |

|

|

|

To Profit transferred to: |

|

|

|

|

|

A's Capital A/c |

18,000 |

|

|

|

|

B's Capital A/c |

9,000 |

27,000 |

|

|

|

|

35,000 |

|

35,000 |

|

|

Partners' Capital Account |

|||||||

|

Dr. |

|

|

|

|

|

|

Cr. |

|

Particulars |

A |

B |

C |

Particulars |

A |

B |

C |

|

To Balance c/d |

2,38,000 |

1,79,000 |

1,00,000 |

By Balance b/d |

1,80,000 |

1,50,000 |

|

|

|

|

|

|

By Bank A/c |

|

|

1,00,000 |

|

|

|

|

|

By Premium for Goodwill A/c |

40,000 |

20,000 |

|

|

|

|

|

|

By Revaluation A/c |

18,000 |

9,000 |

|

|

|

|

|

|

|

|

|

|

|

|

2,38,000 |

1,79,000 |

1,00,000 |

|

2,38,000 |

1,79,000 |

1,00,000 |

|

Balance Sheet as on March 31, 2016 |

|||||

|

Dr. |

|

|

|

Cr. |

|

|

Liabilities |

|

Rs. |

Assets |

|

Rs. |

|

Bills Payable |

|

10,000 |

Cash in Hand |

|

10,000 |

|

Creditors |

|

59,000 |

Cash at Bank |

|

2,00,000 |

|

Outstanding Expenses |

|

2,000 |

Sundry Debtors |

60,000 |

|

|

Capital Account: |

|

|

Less: Provision for Doubtful Debt |

3,000 |

57,000 |

|

A |

2,38,000 |

|

Stock |

|

36,000 |

|

B |

1,79,000 |

|

Plant |

|

1,20,000 |

|

C |

1,00,000 |

5,17,000 |

Buildings |

|

1,65,000 |

|

|

|

5,88,000 |

|

|

5,88,000 |

Working Notes:

1. Sacrificing Ratio = Old Ratio -New Ratio

Sacrificing Ratio between A and B = 2:1.

Reconstitution of a Partnership Firm - Admission of a Partner Exercise 163

Solution NUM 28

|

Books of Leela, Meeta and Om Journal Entries |

|||||

|

Date |

Particulars |

|

L.F. |

Dr. Rs. |

Cr. Rs. |

|

2007 |

|

|

|

|

|

|

Jan 01 |

General Reserve A/c |

Dr. |

|

16,000 |

|

|

|

Profit and Loss A/c |

Dr. |

|

24,000 |

|

|

|

------To Leela's Capital A/c |

|

|

|

25,000 |

|

|

------To Meeta's Capital A/c |

|

|

|

15,000 |

|

|

(Being general reserve and balance in profit and loss account credited to old partners' capital account in old ratio i.e., 5:3) |

|

|

|

|

|

|

|

|

|

|

|

Solution NUM 29

|

Books of Amit, Viney and Ranjan Journal Entries |

|||||

|

Date |

Particulars |

|

L.F. |

Dr. Rs. |

Cr. Rs. |

|

2017 |

|

|

|

|

|

|

Jan 01 |

Amit's Capital A/c |

Dr. |

|

30,000 |

|

|

|

Viney's Capital A/c |

Dr. |

|

10,000 |

|

|

|

------To Profit and Loss A/c |

|

|

|

40,000 |

|

|

(Being debit balance in profit and loss account written off in old ratio) |

|

|

|

|

|

|

|

|

|

|

|

Solution NUM 30

|

Books of A, B and C Journal Entries |

|||||

|

Date |

Particulars |

|

L.F. |

Dr. Rs. |

Cr. Rs. |

|

2016 |

|

|

|

|

|

|

April 01 |

Bank A/c |

Dr. |

|

15,000 |

|

|

|

------To C's Capital A/c |

|

|

|

10,000 |

|

|

------To Premium for Goodwill A/c |

|

|

|

5,000 |

|

|

(Being capital and premium for goodwill brought by C for 1/5th Share) |

|

|

|

|

|

|

|

|

|

|

|

|

April 01 |

Premium for Goodwill A/c |

Dr. |

|

5,000 |

|

|

|

------To A's Capital A/c |

|

|

|

3,750 |

|

|

------To B's Capital A/c |

|

|

|

1,250 |

|

|

(Being amount of goodwill brought by C is transferred to old partners' capital account in their sacrificing ratio i.e., 3:1) |

|

|

|

|

|

|

|

|

|

|

|

|

April 01 |

A's Capital A/c |

Dr. |

|

1,875 |

|

|

|

B's Capital A/c |

Dr. |

|

625 |

|

|

|

------To Bank A/c |

|

|

|

2,500 |

|

|

(Being half of amount of goodwill withdrawn by old partners) |

|

|

|

|

|

|

|

|

|

|

|

|

April 01 |

Revaluation A/c |

Dr. |

|

4,050 |

|

|

|

------To Stock A/c |

|

|

|

2,000 |

|

|

------To Fixture A/c |

|

|

|

100 |

|

|

------To Provision for doubtful Debts on Debtors A/c |

|

|

|

800 |

|

|

------To Provision for doubtful Debts on Bills Receivable A/c |

|

|

|

150 |

|

|

------To Claim for damages A/c |

|

|

|

1,000 |

|

|

(Being revaluation of assets and liabilities) |

|

|

|

|

|

|

|

|

|

|

|

|

April 01 |

Land and Building A/c |

Dr. |

|

5,000 |

|

|

|

Sundry Creditors A/c |

Dr. |

|

650 |

|

|

|

------To Revaluation A/c |

|

|

|

5,650 |

|

|

(Being revaluation of assets and liabilities) |

|

|

|

|

|

|

|

|

|

|

|

|

April 01 |

Revaluation A/c |

Dr. |

|

1,600 |

|

|

|

------To A's Capital A/c |

|

|

|

1,200 |

|

|

------To B's Capital A/c |

|

|

|

400 |

|

|

(Being profit on Revaluation transferred to old partners' capital) |

|

|

|

|

|

|

|

|

|

|

|

|

April 01 |

Reserve Fund A/c |

Dr. |

|

4,000 |

|

|

|

------To A's Capital A/c |

|

|

|

3,000 |

|

|

------To B's Capital A/c |

|

|

|

1,000 |

|

|

(Being reserve fund distributed among old partners) |

|

|

|

|

|

|

|

|

|

|

|

|

Balance Sheet as on April 01, 2016 |

||||||||

|

Dr. |

|

|

|

Cr. |

||||

|

Liabilities |

Rs. |

Assets |

Rs. |

|||||

|

Sundry Creditors |

|

40,850 |

Cash at Bank |

|

39,000 |

|||

|

Claim for Damages |

|

1,000 |

Bills Receivable |

3,000 |

|

|||

|

A |

36,075 |

|

Less: Provision for doubtful Debts on Debtors |

150 |

2,850 |

|||

|

B |

18,025 |

|

Debtors |

16,000 |

|

|||

|

C |

10,000 |

64,100 |

Less: Provision doubtful Debts on Bills Receivable |

800 |

15,200 |

|||

|

|

|

|

Stock |

|

18,000 |

|||

|

|

|

|

Fixtures |

|

900 |

|||

|

|

|

|

Land and Buildings |

|

30,000 |

|||

|

|

|

1,05,950 |

|

|

1,05,950 |

|||

Working Note:

1.

|

Revaluation Account |

||||

|

Dr. |

|

|

|

Cr. |

|

Particulars |

|

Rs. |

Particulars |

Rs. |

|

To Stock A/c |

|

2,000 |

By Land and Building A/c |

5,000 |

|

To Fixture A/c |

|

100 |

By Sundry Creditors A/c |

650 |

|

To Provision for doubtful Debts on Debtors A/c |

|

800 |

|

|

|

To Provision for doubtful Debts on Bills Receivable A/c |

|

150 |

|

|

|

To Claim for damages A/c |

|

1,000 |

|

|

|

To Profit transferred to |

|

|

|

|

|

A's Capital |

1,200 |

|

|

|

|

B's Capital |

400 |

1,600 |

|

1,600 |

|

|

|

5,650 |

|

5,650 |

2.

|

Partners' Capital Account |

|||||||

|

Dr. |

|

|

|

|

|

|

Cr. |

|

Particulars |

A |

B |

C |

Particulars |

A |

B |

C |

|

To Bank A/c |

1,875 |

625 |

|

By Balance b/d |

30,000 |

16,000 |

|

|

To Balance c/d |

36,075 |

18,025 |

10,000 |

By Bank A/c |

|

|

10,000 |

|

|

|

|

|

By Premium for Goodwill A/c |

3,750 |

1,250 |

|

|

|

|

|

|

By Revaluation A/c |

1,200 |

400 |

|

|

|

|

|

|

By Reserve Fund A/c |

3,000 |

1,000 |

|

|

|

37,950 |

18,650 |

10,000 |

|

37,950 |

18,650 |

10,000 |

3.

|

Bank Account |

|||

|

Dr. |

|

|

Cr. |

|

Particulars |

Rs. |

Particulars |

Rs. |

|

To Balance b/d |

26,500 |

By A's Capital A/c |

1,875 |

|

To C's capital A/c |

10,000 |

By B's Capital A/c |

625 |

|

To Premium for Goodwill A/c |

5,000 |

By Balance c/d |

39,000 |

|

|

|

|

|

|

|

|

|

|

|

|

41,500 |

|

41,500 |

- Assuming that ratio between A and B has not change hence sacrificing ratio should be same as old ratio.

Sacrificing Ratio = Old Ratio -New Ratio

Reconstitution of a Partnership Firm - Admission of a Partner Exercise 164

Solution NUM 31

|

Books of A, B and C Journal Entries |

|||||

|

Date |

Particulars |

|

L.F. |

Dr. Rs. |

Cr. Rs. |

|

2017 |

|

|

|

|

|

|

Apr 01 |

A's Capital A/c |

Dr. |

|

5,000 |

|

|

|

------To Cash A/c |

|

|

|

5,000 |

|

|

(Being excess capital withdrawn by A) |

|

|

|

|

|

|

|

|

|

|

|

|

|

Cash A/c |

Dr. |

|

3,000 |

|

|

|

------To B's Capital A/c |

|

|

|

3,000 |

|

|

(Being capital brought in by B to make in proportion to the profit sharing) |

|

|

|

|

|

|

|

|

|

|

|

1. Calculation of New Profit sharing Ratio

New profit sharing ratio of A, B and C will be 9:3:4

2. New capital of A and B.

C bring Rs.20,000 for 1/4th share of profit in the new firm.

![]()

Solution NUM 32

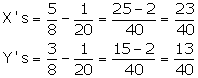

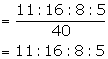

1. Calculation of new profit sharing Ratio = Old Ratio - Sacrificing Ratio

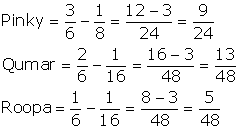

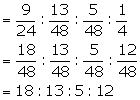

New profit sharing ratio between Pinky, Qumar, Roopa and Seema

2. Required capital of all partners in the new firm

3. Amount to be brought by each partner

Pinky = 90,000 - 80,000 =10,000

Qumar = 65,000 - 30,000 =35,000

Roopa = 25,000 - 20,000 =5,000

![]()

|

Books of Pinky, Qumar, Roopa and Seema Journal Entries |

|||||

|

Date |

Particulars |

|

L.F. |

Dr. Rs. |

Cr. Rs. |

|

|

Bank A/c |

Dr. |

|

60,000 |

|

|

|

------To Seema Capital A/c |

|

|

|

60,000 |

|

|

(Being seema bring her share of Capital) |

|

|

|

|

|

|

|

|

|

|

|

|

|

Bank A/c |

Dr. |

|

50,000 |

|

|

|

------To Pinky's Capital A/c |

|

|

|

10,000 |

|

|

------To Qumar's Capital A/c |

|

|

|

35,000 |

|

|

------To Roopa's Capital A/c |

|

|

|

5,000 |

|

|

(Being amount brought by Pinky, Qumar and Roopa to make capital equal to their proportion) |

|

|

|

|

|

|

|

|

|

|

|

Solution NUM 33

|

Books of Arun, Bablu, Chetan and Deepak Profit and Loss Adjustment Account (Revaluation Account) |

||||

|

Dr. |

|

|

Cr. |

|

|

Particulars |

Rs. |

Particulars |

Rs. |

|

|

To Furniture |

|

420 |

By Buildings |

7,000 |

|

To Stock |

|

1,400 |

|

|

|

To Reserve for Doubtful Debts |

|

630 |

|

|

|

To Profit on revaluation |

|

|

|

|

|

To Profit transferred to: |

|

|

|

|

|

Arun's Capital |

1,950 |

|

|

|

|

Bablu's Capital |

1,625 |

|

|

|

|

Chetan's Capital |

975 |

4,550 |

|

|

|

|

7,000 |

|

7,000 |

|

|

Cash Account |

|||

|

Dr. |

|

|

Cr. |

|

Particulars |

Rs. |

Particulars |

Rs. |

|

To Balance b/d |

900 |

By Arun's Capital A/c |

1,750 |

|

To Chetan's capital A/c |

625 |

By Bablu's Capital A/c |

1,625 |

|

To Deepak's Capital A/c |

7,000 |

By Balance c/d |

9,350 |

|

To Primum for Goodwill |

4,200 |

|

|

|

|

|

|

|

|

|

12,725 |

|

12,725 |

|

Balance Sheet |

||||||||

|

Dr. |

|

|

|

Cr. |

||||

|

Liabilities |

Rs. |

Assets |

Rs. |

|||||

|

Creditors |

|

9,000 |

Land and Buildings |

|

31,000 |

|||

|

Bills Payable |

|

3,000 |

Furniture |

|

3,080 |

|||

|

Capital Accounts |

|

|

Stock |

|

12,600 |

|||

|

Arun |

21,000 |

|

Debtors |

12,600 |

|

|||

|

Bablu |

17,500 |

|

Less: Reserve for Doubtful Debt |

630 |

11,970 |

|||

|

Chetan |

10,500 |

|

Cash |

|

9,350 |

|||

|

Deepak |

7,000 |

56,000 |

|

|

|

|||

|

|

|

|

|

|

|

|||

|

|

|

68,000 |

|

|

68,000 |

|||

Working Note:

1.

|

Partners' Capital Account |

|||||||||

|

Dr. |

|

|

|

|

|

|

|

|

Cr. |

|

Particulars |

Arun |

Bablu |

Chetan |

Deepak |

Particulars |

Arun |

Bablu |

Chetan |

Deepak |

|

To Bank A/c |

1,750 |

1,625 |

|

|

By Balance b/d |

19,000 |

16,000 |

8,000 |

|

|

To Balance c/d |

21,000 |

17,500 |

10,500 |

7,000 |

By Cash A/c |

|

|

|

7,000 |

|

|

|

|

|

|

By Premium for Goodwill A/c |

1,800 |

1,500 |

900 |

|

|

|

|

|

|

|

By Revaluation A/c |

1,950 |

1,625 |

975 |

|

|

|

|

|

|

|

By Bank A/c |

|

|

625 |

|

|

|

22,750 |

19,125 |

10,500 |

7,000 |

|

22,750 |

19,125 |

10,500 |

7,000 |

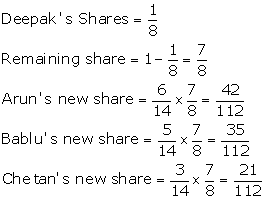

2. Calculation of New Profit sharing Ratio

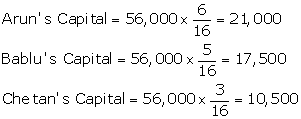

New profit sharing ratio of Arun, Bablu, Chetan and Deepak

3. Calculation of Capital of Arun, Bablu and Chetan in the firm

![]()

![]()

Reconstitution of a Partnership Firm - Admission of a Partner Exercise 165

Solution NUM 34

|

Books of Azad, Babli and Chintan Journal Entries |

|||||

|

Date |

Particulars |

|

L.F. |

Dr. Rs. |

Cr. Rs. |

|

2016 |

|

|

|

|

|

|

Mar 31 |

Bank A/c |

Dr. |

|

42,000 |

|

|

|

------To Chintan's Capital A/c |

|

|

|

30,000 |

|

|

------To Premium for Goodwill A/c |

|

|

|

12,000 |

|

|

(Being Chintan brought capital and premium for Goodwill for 1/4 share of profit) |

|

|

|

|

|

|

|

|

|

|

|

|

|

Premium for Goodwill A/c |

Dr. |

|

12,000 |

|

|

|

------To Azad's Capital A/c |

|

|

|

8,000 |

|

|

------To Babli's Capital A/c |

|

|

|

4,000 |

|

|

(Being goodwill brought by Chintan transferred to old partners capital account in their sacrificing ratio i.e., 2:1) |

|

|

|

|

|

|

|

|

|

|

|

|

|

General Reserve A/c |

Dr. |

|

6,000 |

|

|

|

------To Azad's Capital A/c |

|

|

|

4,000 |

|

|

------To Babli's Capital A/c |

|

|

|

2,000 |

|

|

(Being general reserve distributed between old partners) |

|

|

|

|

|

|

|

|

|

|

|

|

|

Building A/c |

Dr. |

|

5,000 |

|

|

|

------To Revaluation A/c |

|

|

|

5,000 |

|

|

(Being increase in value of Building adjusted) |

|

|

|

|

|

|

|

|

|

|

|

|

|

Revaluation A/c |

Dr. |

|

2,480 |

|

|

|

------To Machinery A/c |

|

|

|

2,000 |

|

|

------To Provision for Doubtful Debt A/c |

|

|

|

480 |

|

|

(Being decrease in value of machinery adjusted and Provision for Doubtful Debt created) |

|

|

|

|

|

|

|

|

|

|

|

|

|

Revaluation A/c |

Dr. |

|

2,520 |

|

|

|

------To Azad's Capital A/c |

|

|

|

1,680 |

|

|

------To Babli's Capital A/c |

|