Class 11-commerce NCERT Solutions Business Studies Chapter 1: Nature and Purpose of Business

Nature and Purpose of Business Exercise 26

Solution SA 1

Trade centers in ancient India:

Patliputra: Major centre of export of stones

Taxila: City of financial and commercial banks

Indrapastha: Commercial junction for roads

Mathura: Emporium of trade and commerce

Peshawar: Export and import centre for wool and horse respectively

Varanasi: Major centre for textile industry and gained fame for the gold silk cloth

Ujjain: Export centre for carnelian, muslin and mallow cloth

Surat: Emporium of western trade and famous for gold zari borders

Kanchi: Hub for Chinese traders who purchased glass, pearls rare stones etc.

Broach: Greatest seat for commerce due to its connection with all other important trade centers via roads

Kaveripatta: Headquarters for foreign traders and trade centre for items like pearl, gold, corals, cotton etc.

Tamralipti: One of the greatest ports connected by sea and land

Solution SA 2

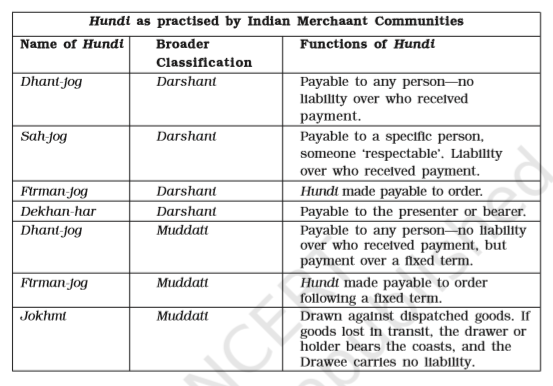

Documents such as Hundi were in use for carrying out transactions in which money passed from hand to hand. Hundi as an instrument of exchange, which was prominent in the subcontinent. It involved a contract which — (i) warrant the payment of money, the promise or order which is unconditional (ii) capable of change through transfer by valid negotiation.

Solution SA 3

Major exports and imports in ancient India are as follows:

Imports: Copper, lead, animal products, horses, gold silver, coral, glass, tin etc.

Exports: Sugar, indigo, cotton, spices, opium, wheat, seasame oil, crystal, granites, copper etc.

Solution SA 4

Solution SA 5

Maritime trade was another important branch of global trade network. Malabar Coast, on which Muziris is situated, has a long history of international maritime trade going back to the era of the Roman Empire. Pepper was particularly valued in the Roman Empire and was known as ‘Black Gold’. For centuries, it remained the reason for rivalry and conflict between various empires and trade powers to dominate the route for this trade. It was in the search for an alternate route to India for spices that led to the discovery of America by Columbus in the closing years of 15th century and also brought Vasco da Gama to the shores of Malabar in 1498.

Solution SA 6

Economic activities involve production, distribution, exchange and consumption of services and goods to consumers. Our livelihoods depend on these activities.

The different types of economic activities are as follows:

- Business: It refers to all those activities which are concerned with production, purchase, sale and supply of goods and services on a regular basis. The main motive of any business is to earn maximum amount of profit.

- Profession: A profession is an occupation where individuals with specialised knowledge and qualification provide specialised services in the relevant field to the masses to earn a living. Each profession is distinct from the other.

- Employment: People are hired to work regularly by organisations. Salaries or wages are paid to employees in exchange for the working hours which they provide to a company.

Solution SA 7

Business is considered an economic activity because it is undertaken to earn money or livelihood. The motive of business is to earn maximum amount of profit and not psychological satisfaction.

Solution SA 8

Human beings, in order to earn a living, indulge themselves in various economic activities. Business, being an economic activity, is all about production, purchase, sale and supply of goods and services. The principle motive behind engaging in a business is to earn adequate amount of profit. A businessman produces goods and services which are in demand so that he/she can earn maximum amount of profit.

Solution SA 9

Business activities are categorised as follows:

- Industry: It refers to economic activities involving that constituent of production where raw materials undergo change and get converted to finished products. It creates form utility as form of raw materials is converted to useful finished products. It is also the group of firms producing the same type of goods. For example, the sugar industry comprises all the firms producing sugar. Industries are again classified into three categories-primary, secondary and tertiary.

- Commerce: After manufacturing and production, comes the task of distribution of goods. Activities which fall under the purview of commerce involve helping directly or indirectly in distributing goods and services from the producers to the users or ultimate consumers. Sometimes, high-in-demand goods are produced at one place and needs to be circulated and distributed to consumers living at different places. In such situations, commerce or commercial activities take a lead in distributing and delivering the goods. Thus, the major commercial activities are transport, advertisement, packaging, warehousing, banking and communication. Hence, we can say that the gap between producers and consumers is removed by commerce. Commerce can then be further classified into trade and auxiliaries to trade.

Solution SA 10

Industries refers to economic activities involving processing and converting of raw materials into final products, either for the use of customers or to satisfy the needs of other industries for further production. The various types of industries are

- Primary industries: Activities related to extraction and production of natural resources and reproduction and development of living species are undertaken. Farming, mining, lumbering, hunting, fishing operations, breeding farms and poultry farms are examples of primary industries. These industries are classified into extractive industries and genetic industries.

- Secondary industries: The final products of primary industries are processed and converted to final goods by secondary industries. Iron mining belongs to primary industries, whereas manufacturing of steel falls under secondary industries. Secondary industries are further classified as manufacturing industries and construction industries.

- Tertiary industries: These industries act as a service provider for the primary and secondary industries and for trade-related activities. Examples of these industries are transport, banking, insurance, warehousing and advertising.

Solution SA 11

Two business activities which are auxiliaries to trade:

- Transport and Communication: Production and consumption of goods take place at different locations. Thus, it is essential to move goods from the place of production to the place of consumption. Transport facilitates this movement and transfers raw materials to the place of production. In addition to transport facility, communication is required so that information can be exchanged between producers, traders and consumers.

- Banking and Finance: A business cannot get going unless funds and investments are available for purchasing raw materials and meeting day-to-day expenses. It can obtain funds from banks and financial institutions by taking loans, and thus, banks overcome the business' problem of funds. Banks help businessmen in internal and external trade.

Solution SA 12

Although there are a couple of main objectives for business, earning profit is the sole motive of any business activity. A business earns profit for various reasons:

- Survival and source of income: Profit is the source of income for a business to flourish and is also a business's lifeline. It satisfies business needs so that they can survive in the competitive market.

- Expansion, growth and continuity of business: Only the incentives from profits can keep a business going and indulging in all its related activities. If a large chunk of the profit is re-invested for expansion and diversification of production, then that business can have a sound footing in the market. Index of performance or measure of efficiency: Profit acts as an index of performance, i.e. the profit earnings will give an overall picture of how the business is functioning in the market. High or adequate amounts of profits indicate efficient management and lower profits or consistent losses indicate inefficiency of the management.

- Reward for bearing risks: Profits are the rewards for bearing the risks and bringing in new products or processes to the market. The desire to earn profit motivates the business to successfully undertake all the risks and invests money.

- Goodwill: Profits and goodwill go hand-in-hand. A profit-earning firm has a better reputation/goodwill in the market as compared to those businesses which are in loss. The share value of a business increases with an increase in profit. High-profit earning firms are more prone to get and raise loans and obtain credit than the ones which lag behind in profit earning. If a business is not earning profits, then it is considered a non-viable venture.

Solution SA 13

Business risk may be defined in terms of the possibility of occurrence of losses or insufficient profits because of various unexpected events which cannot be controlled by business.

For example, customer preference for a certain product declines after a certain period because of some competitors' policies or change in taste; in such cases, it is extremely difficult for a businessperson to correctly anticipate consumer preferences, as a result of which he or she always faces the risk of unforeseen fluctuations in demand. This results in the business going into a loss because of the fall in demand.

Nature of business risk:

- Essential part of business: Risk is an essential part of business and cannot be avoided. Every type of business faces risk although the degree of risk may vary. A business risk can be reduced but cannot be eliminated.

- Depends on the nature of business: The degree of risk which a business faces depends on the nature and size of the business. A large-scale business is more prone to risks than a small-scale one. For instance, a business which produces goods of daily use, such as soap and toothpaste, faces a lower business risk than a business which produces fashion goods which are highly dependent on consumer preferences.

- Profit-the reward for bearing risk: A business earns profit for undertaking risk. 'No pain, no gain' goes hand-in-hand with 'no risk, no gain' in business. Higher the degree of risk involved, higher the amount of profit earned and vice versa.

- Arise due to uncertainties: Change in government policies or natural calamities can be some uncertain reasons which can cause a business risk as the outcome of such events are unknown to all.

Solution LA 1

Indigenous banking system is a banking system developed in ancient times wherein individuals or private firms (also known as indigenous bankers) performed various functions like accepting deposits, lending money by way of currency or letter of credit etc.

As economic life progressed, metals began to supplement other commodities as money because of its durability and divisibility. As money served as a medium of exchange, the introduction of metallic money and its use accelerated economic activities. Documents such as Hundi and Chitti were in use for carrying out transactions in which money passed from hand to hand. Hundi as an instrument of exchange, which was prominent in the subcontinent. It involved a contract which — (i) warrant the payment of money, the promise or order which is unconditional (ii) capable of change through transfer by valid negotiation. Indigenous banking system played a prominent role in lending money and financing domestic and foreign trade with currency and letter of credit. With the development of banking, people began to deposit precious metals with lending individuals functioning as bankers or Seths, and money became an instrument for supplying the manufacturers with a means of producing more goods.

Agriculture and the domestication of animals were important components of the economic life of ancient people. Due to the favourable climatic conditions they were able to raise two or sometimes three crops in a year. In addition to this, by resorting to weaving cotton, dyeing fabrics, making clay pots, utensils, and handicrafts, sculpting, cottage industries, masonry, manufacturing, transports (i.e., carts, boats and ships), etc., they were able to generate surpluses and savings for further investment.

Workshops (Karkhana) were prominent where skilled artisans worked and converted raw materials into finished goods which were high in demand. Family-based apprenticeship system was in practice and duly followed in acquiring trade-specific skills. The artisans, craftsmen and skilled labourers of different kinds learnt and developed skills and knowledge, which were passed on from one generation to another.

Solution LA 2

Human beings, in order to earn a living, indulge themselves in various economic activities. Business, being an economic activity, is all about production, purchase, sale and supply of goods and services. The principle motive behind engaging in a business is to earn adequate amount of profit. A businessman produces goods and services which are in demand so that he/she can earn maximum amount of profit.

The characteristics of business are as follows:

- Economic activity: Business is conducted by entrepreneurs to earn an adequate amount of profit and not to fulfil psychological needs. Thus, we can conclude that it is an economic activity.

- Production or procurement of goods and services: Business involves procurement of raw materials and semi-finished goods and services. It either manufactures the goods or acquires them from producers and thereafter sells to the final consumers at higher prices.

- Profit earning: Profit is the purpose of a business. A business can sustain and grow only if it is earning a good amount of profit. If the profit motive is missing in a transaction, then it cannot be considered a business activity.

- Sale or exchange of goods and services: Business involves the sale or exchange of goods and services between the seller and buyer for value. Thus, production of goods for self-consumption will not be considered business, but if production of goods is for sale in the market, then it will be called business.

- Dealings in goods and services regularly: Business basically involves an exchange of goods and services done regularly. One single transaction of sale does not constitute a business. Business transactions regularly are a must for the business to survive.

- Risk element: Business risk may be defined in terms of the possibility of occurrence of losses or insufficient profits because of various unexpected events which cannot be controlled by business. Every type of business faces risk although the degree of risk may vary from business to business. A business risk can be reduced but cannot be eliminated.

- Uncertainty of return: Uncertainty of return means lack of knowledge regarding the returns on investment. That is, a businessman does not know the amount of profit which he will be earning in the future.

Solution LA 3

|

|

Basis |

Business |

Profession |

Employment |

|

i. |

Commencement |

By an entrepreneur and after the fulfilment of certain legal formalities |

After the completion of a professional degree or a course from an institute |

After receiving an appointment letter and service agreement |

|

ii. |

Capital investment |

Depends on the scale and nature of the business |

Limited capital investment is required |

No capital investment is required |

|

iii. |

Risk |

Risk and uncertainty are always there |

A comparatively low degree of risk is involved |

Negligible risk involved |

|

iv. |

Transfer of ownership |

Possible on fulfilment of certain legal formalities |

Not possible as professional has the required degree and skills which cannot be transferred to the other person |

Not possible |

|

v. |

Reward |

Profit earned |

Professional fees |

Salary or wages |

|

vi. |

Code of conduct |

No code of conduct |

Prescribed by professional associations |

According to the terms and conditions laid down by the concerned organisation |

|

vii. |

Qualification |

No minimum qualification is necessary |

Prescribed professional qualification is necessary |

Depends on the nature of the job |

Solution LA 4

Following are the various types of industries:

- Primary industries: Under these industries, activities related to extraction and production of natural resources and reproduction and development of living species are undertaken. Farming, mining, lumbering, hunting, fishing operations, breeding farms and poultry farms are examples of primary industries. These industries are classified into extractive industries and genetic industries.

- Extractive industries: Products are extracted from natural resources such as soil and water. Manufacturing industries convert the products of these industries into useful goods. Examples: Farming, mining, lumbering, hunting and fishing operations

- Genetic industries: They include breeding and reproduction of plants and animals. Examples: Cattle breeding farms, poultry farms, fishing hatcheries

- Secondary industries: The final products of primary industries are processed and converted to final goods by secondary industries. Iron mining belongs to the primary industries, whereas manufacturing of steel falls under secondary industries. Secondary industries are further classified as manufacturing industries and construction industries.

- Manufacturing industries: These industries convert raw materials or semi-finished products into finished products. For example, sugarcane is converted to sugar. These industries are divided into the following categories.

1. Analytical industry: A raw material is analysed and separated into different products. Example: Oil refinery

2. Synthetic industry: Different raw materials are combined to produce a new product. Examples: Cement industry, cosmetic industry

3. Processing industry: This industry involves successive stages in order to produce the product. Examples: Sugar industry, paper industry

4. Assembling industry: different parts are assembled to make a new product. Examples: Television, car, washing machine, computer

- Construction industries: These industries are engaged in construction of buildings, dams, roads and bridges. These industries require engineering and architectural skills.

- Tertiary industries: These industries act as a service provider for the primary and secondary industries and for trade-related activities. Examples: Transport, banking, insurance, warehousing, advertising

Solution LA 5

Activities related to commerce are trade and auxiliaries to trade.

- Trade: It refers to buying and selling of goods and services. It is only through trade that goods are made available to consumers from manufacturers. Trade can be classified into two types:

- Internal trade: When the trade occurs within the geographical boundaries of the country, it is called internal/home/domestic trade. It is further classified into wholesale and retail trade.

i. Wholesale trade: It is concerned with buying and selling of goods in large scale.

ii. Retail trade: It is concerned with buying and selling of goods in smaller quantities.

- External trade: When trade occurs beyond the geographical boundaries of the country between people and organisations, it is called external trade. External trade can be classified into import, export and entrepôt.

i. Import trade: Goods purchased from foreign countries come under import trade.

ii. Export trade: Goods sold to foreign countries fall under export trade.

iii. Entrepôt trade: Importing goods for exporting them to the other country again is termed entrepôt trade.

- Auxiliaries to trade: It refers to those activities which support trade. Generally, these activities are called services as they eliminate various hindrances which take place when goods are produced and distributed. The following are the auxiliaries to trade.

- Transport and Communication: Production and consumption of goods take place at different locations. Thus, it is essential to move goods from the place of production to the place of consumption. Transport facilitates this movement and transfers raw materials to the place of production. In addition to transport facility, communication is required so that information can be exchanged between producers, traders and consumers.

- Banking and Finance: A business cannot be get going unless funds and investments are available for purchasing raw materials and meeting day-to-day expenses. It can obtain funds from banks and financial institutions by taking loans, and thus, banks overcome the business’ problem of funds. Banks help businessmen in internal and external trade.

- Insurance: We know that every kind of business involves various types of risks such as risk of loss due to fire, theft and damage and risk of accident. To be protected from such risks, a business can opt for insurance. Insurance provides protection from all kinds of risks and in return charges fees (which is called premium).

- Warehousing: Production and consumption of goods do not take place simultaneously. There is a time gap between them. Hence, some place is needed to store the goods before supplying them to the ultimate consumers.

- Advertising: It is one of the tools used to promote a product. Promotion of the product helps in increasing its sales. Advertising informs customers about the features of a product and convinces them to buy it.

Solution LA 6

Objectives are the end towards which all the business activities are directed to. Although the sole objective of every business is to earn maximum amount of profit, with growing competition and diversity, multiple objectives have been put in place. All the efforts of a business are then guided to achieve those objectives.

Keeping the prime objective in mind, a business strives to achieve the following objectives:

- Market standing: It means position of the firm in the market. A firm can build a strong position in the market by providing a good quality product to its customers and offering certain other product-related benefits.

- Innovation: It refers to the development or invention of new ideas, techniques and methods to meet new demands of the flourishing business and competitive market. It is an important objective of business as no business can survive in the market without innovation.

- Productivity: It is calculated by making comparison between output and input. Efficiency is measured through productivity. To survive and grow, it is essential for the organisation to be productive.

- Maximum profit: Profit is the excess of revenue over cost. The purpose of every business is to earn adequate amount of profit. A business can sustain and grow only if it is earning a good amount of profit.

Physical and financial resources: Physical resources such as plants, machines, furniture and office and financial resources (i.e. funds) are required by every business organisation to run the organisation.

Solution LA 7

Business risk may be defined in terms of the possibility of occurrence of losses or insufficient profits because of various unexpected events which cannot be controlled by business.

For example, customer preferences for a certain product declines after a certain period because of some competitors' policies or change in taste; in such cases, it is extremely difficult for a businessperson to correctly anticipate consumer preferences, as a result of which he or she always faces the risk of unforeseen fluctuations in demand. This results in the business going for a loss because of the fall in demand.

Two types of business risks are speculative risk and pure risk.

- Speculative risk: Risks taken on the basis of forecasts and guesses can be termed speculative risk. It involves an equal possibility of earning gains or incurring losses. It arises because of change in market conditions like changes in government policies and fluctuation in demand and supply.

- Pure risk: Risks which cannot be predicted precisely is pure risk. A firm can incur only losses or incur no loss at all. Pure risk can be the risk associated with theft, fire and various natural calamities.

Causes of business risk:

- Natural causes: The one thing which humans have no control over is nature. So, when unforeseen natural calamities occur, it causes heavy and irreplaceable losses to life, property and income.

- Economic causes: Price fluctuations and change in government policies, preferences, taste and demand of consumers are some of the economic causes which will cause the downfall of a business.

- Human causes: One of the common causes of business loss is humans. For example, dishonest behaviour of employees, carelessness of employees and strikes.

- Other causes: Political disturbances, exchange-rate and interest-rate fluctuations, budget amendments, physical or technical disabilities and mechanical failures can be some other causes which may result in a business risk.

Solution LA 8

Factors to be considered while starting a business:

- Selecting a business line: The basic decision which needs to be taken at the start is choosing a line of business. This decision is dependent on many factors such as demand of consumers, interest area of entrepreneur and profit margin in the production of a particular product. Besides these, technical knowledge which an entrepreneur has for the production of a particular product influences the selection of a line of business.

- Size of the business: The size of the business, i.e. whether to operate on a large scale or small scale, is also one of the important decisions to be considered while starting a business. A business can be operated on a large scale if the entrepreneur is confident regarding the demand for the product and the capital can be easily arranged. On the contrary, operations will be started on a small scale if the risk is high; there is difficulty in arranging large amount of capital and market conditions are unstable.

- Location: The choice regarding the place of starting a business depends on the following factors.

a) Availability of raw materials and labour

b) Power supply

c) Services such as banking, transport, communication and warehousing

Venturing into a business started at a wrong location will result in high cost of production, inconvenience in getting the right kind of raw materials and low demand.

- Financial requirement: Finance is required at every stage of a business from the start point of business and purchase of fixed assets to continuous investment in the business. In this regard, a proper financial analysis helps determine the required capital amount, capital sources and the best ways to use capital.

- Tax planning: Tax laws influence the profit margin and working of the business. Hence, it becomes essential for the business to do tax planning well in advance.

- Physical facilities: Before starting a business, physical facilities such as machines, equipment, building and other important physical resources should be carefully considered. This is because physical resources add to the efficiency of a business. This decision is based on the nature, size and production process of the business as well as the availability of funds.