CBSE Class 12-commerce Answered

Understanding Receipts and Payments Account:

- Meaning: It is an account that shows the summary of all cash and bank transactions occurred during an accounting period. It starts with the opening balances of cash and bank and ends with the closing balances of cash and bank. This account is a Real Account and lays the basis for the preparation of Income and Expenditure Account and the Balance Sheet.

- Features: Following are the features of Receipts and Payments Account:

- Nature: It is a summary of cash receipts and payments and hence, it an Asset Account/Real Account

- Recording: It provides the summary of all cash and bank transactions in a chronological order.

- Basis of Preparing: It is prepared on cash basis, i.e., it records only cash inflow and outflow. Accrued and outstanding transactions are not recorded in this account.

- Capital and Revenue: It records all the transactions whether capital or revenue.

- Period: It records all the cash and bank transactions irrespective of whether they relate to current, previous or succeeding accounting periods.

- Opening and Closing Balances: Opening balance of this account is the cash in hand/ bank at the beginning of the accounting year and the closing balance shows cash in hand/bank at the end of the accounting period.

- Adjustment: Adjustments for accrued, outstanding items and depreciation is not required to be made in this account.

- Purpose: The purpose of preparing this account is to show amount received and paid under various heads during the accounting year and also to know the cash position of the entity.

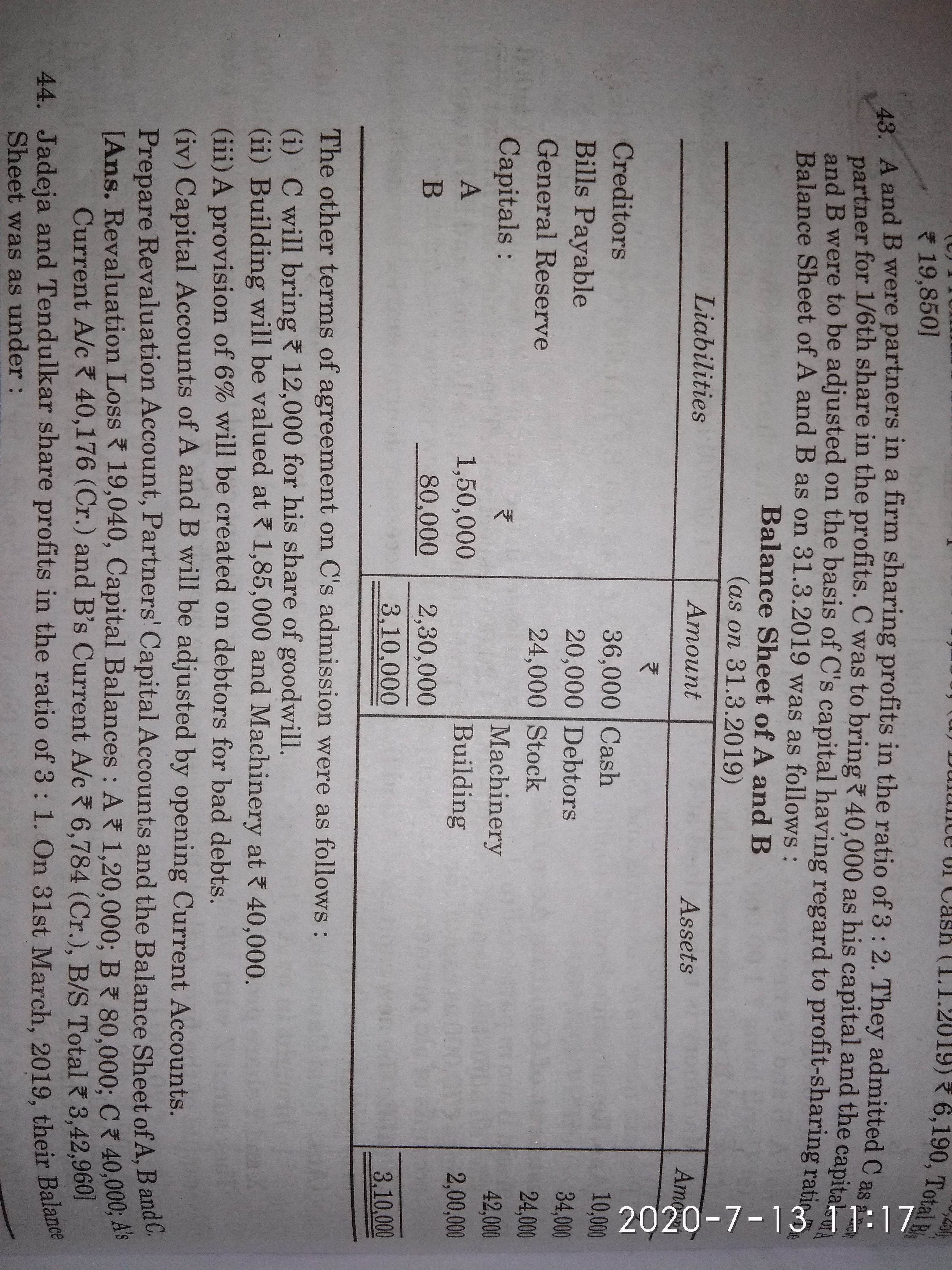

- Format:

Dr. Receipts and Payments Account for the year ended … Cr

|

Receipts |

Amount |

Payments |

Amount |

|

To Balance b/d(Opening Balance): Cash in Hand Cash at Banks To Subscriptions: For Previous Year … For Current Year … For Next Year … To General Donations To Entrance/Admission Fees To General Grants To Sale of Newspaper, Grass, etc. To Sale of Old Used Sports Materials To Interest on Investments To Income from Concerts/Lectures To Dividends To Rent Received To Interest Received To Miscellaneous Receipts To Life Membership Fees To Subscriptions for Specific Purpose To Donation for Specific Purpose To Legacies To Endowment Fund To Sale of Fixed Assets To Receipts on Account of Special Fund, i.e., Match Fund, Prize Fund, etc. To Balance c/d (Bank Overdraft)* |

… …

… … … … … … … … … … … … … … … … … … …

… |

By Balance b/d (Opening Balance)(in case of Bank Overdraft) By Salaries By Rent By Postage Expenses By Newspapers and Magazines, etc. By Repairs By Audit Fee By Maintenance Expenses By Insurance By Secretary’s Honorarium By Honorarium By Municipal Tax By Prize Distributed By Office Expenses By Expenses on Show By Miscellaneous Payments By Purchase of Fixed Assets (e.g., Furniture) By Sports Equipment By Investments By Books By Loan (Repayment) By Building By Balance c/d (Closing Balance): Cash in Hand Cash at Bank* |

… … … … …

… … … … … … … … … … … …

… … … … …

… … |

|

|

… |

|

… |

*Either of the two will appear.

# If the receipts side is more than the payments side then, Closing balance of cash and bank will appear on the credit side of this account.

If the payments side is more than the receipts side then, Closing balance of bank will appear (as Bank overdraft) on the debit side of this account.

Application Videos

-

Special Aspects: Salary and Commission ...

This video explains the Meaning and Treatment of Salary and Commission alon...

This video explains the Meaning and Treatment of Salary and Commission alon... -

Meaning and Preparation of Common-Size Statement of Pro ...

This video explains the meaning and preparation of Common-Size Statement of...

This video explains the meaning and preparation of Common-Size Statement of... -

Meaning and Preparation of Common-Size Balance Sheet ...

This video explains the meaning and preparation of Common-Size Balance Shee...

This video explains the meaning and preparation of Common-Size Balance Shee... -

Accounting Treatment of Reserves and Accumulated Profit ...

This video explains the Accounting Treatment of Reserves, Accumulated Profi...

This video explains the Accounting Treatment of Reserves, Accumulated Profi... -

Accounting Treatment of Reserves and Accumulated Profit ...

This video explains the Accounting Treatment of Reserves, Accumulated Profi...

This video explains the Accounting Treatment of Reserves, Accumulated Profi...

Concept Videos

-

Reconstitution: Change in Existing Profit Sharing Ratio ...

Reconstitution: Change in Existing Profit Sharing Ratio, Introduction to Re...

Reconstitution: Change in Existing Profit Sharing Ratio, Introduction to Re... -

Reconstitution: Change in Existing Profit Sharing Ratio ...

Reconstitution: Change in Existing Profit Sharing Ratio, Introduction to Re... -

Reconstitution: Change in Existing Profit Sharing Ratio ...

Reconstitution: Change in Existing Profit Sharing Ratio, Introduction to Re... -

Reconstitution: Change in Existing Profit Sharing Ratio ...

Reconstitution: Change in Existing Profit Sharing Ratio, Introduction to Re... -

Reconstitution: Change in Existing Profit Sharing Ratio ...

Reconstitution: Change in Existing Profit Sharing Ratio, Introduction to Re...