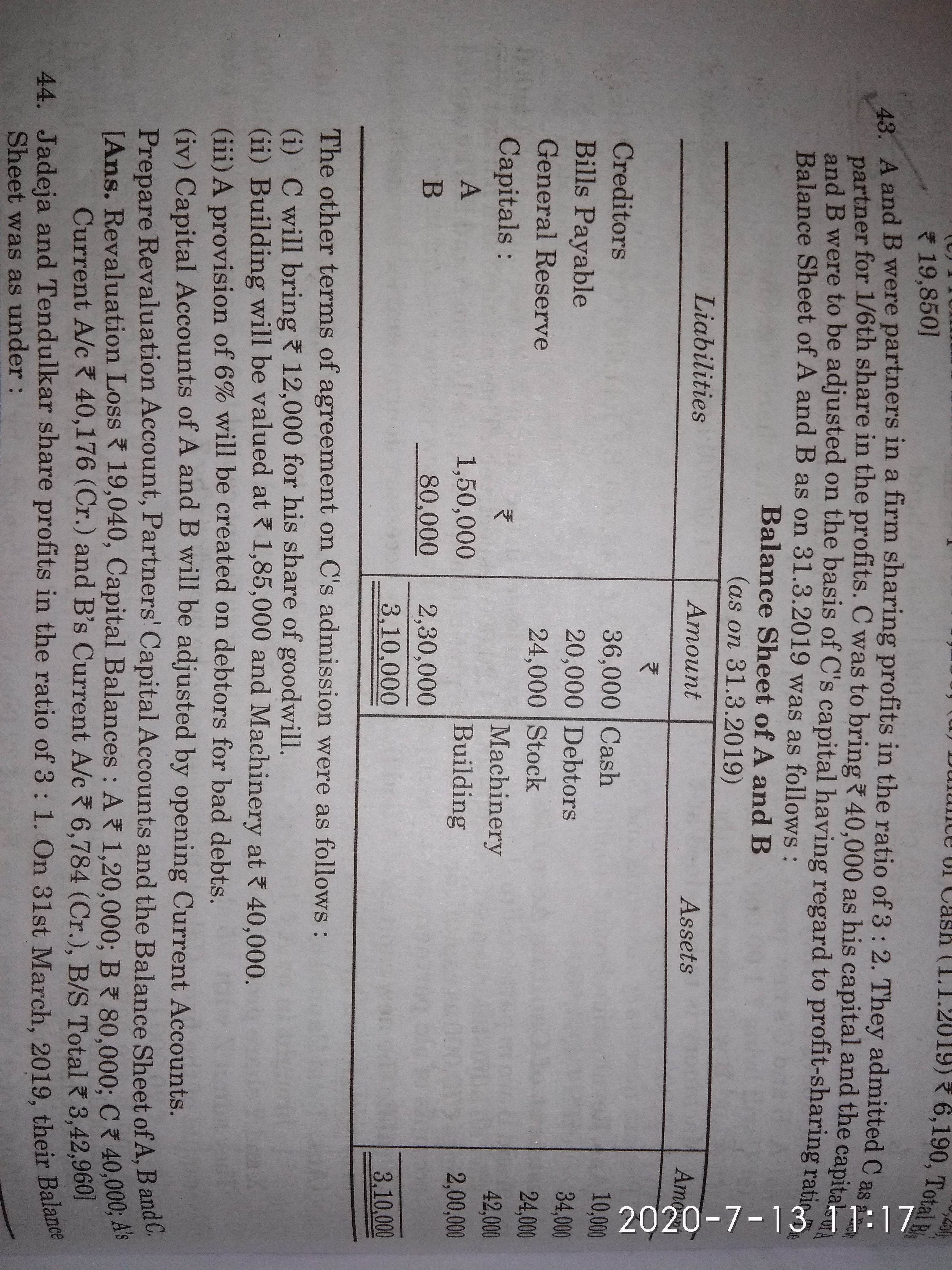

CBSE Class 12-commerce Answered

|

|

Basis |

Profit and Loss Account |

Profit and Loss Appropriation Account |

|

1 |

Stage of Preparation |

It is prepared after Trading Account and therefore, starts with Gross Profit or Gross Loss transferred from the Trading Account. |

It is prepared after Profit and Loss Account and therefore, starts with Net Profit or Net Loss as transferred from the Profit and Loss Account. |

|

2 |

Objective |

It determines net profit earned or net loss incurred during the accounting year. |

It shows appropriation of net profit i.e., distribution of Net Profit for the accounting period among the partners. |

|

3 |

Nature of Items |

It is debited with the expenses and credited with the income, not being business income to determine net profit for accounting period. |

It is debited with the items of appropriation of profit like salary, commission, interest on capital, transfer to reserve, etc. and credited with the items of income being debited to Partners’ Capital Account or Current Accounts such as interest on drawings. |

|

4 |

Partnership Deed |

This account is not guided by the Partnership Deed or Agreement. |

This account is prepared as guided by the Partnership Deed or Agreement or provisions of Indian Partnership Act, 1932. |

|

5 |

Matching Principle |

It follows the Matching Principle where revenue is matched against expense. |

It does not follow the Matching Principle. |

|

|

Basis |

Profit and Loss Account |

Profit and Loss Appropriation Account |

|

1 |

Stage of Preparation |

It is prepared after Trading Account and therefore, starts with Gross Profit or Gross Loss transferred from the Trading Account. |

It is prepared after Profit and Loss Account and therefore, starts with Net Profit or Net Loss as transferred from the Profit and Loss Account. |

|

2 |

Objective |

It determines net profit earned or net loss incurred during the accounting year. |

It shows appropriation of net profit i.e., distribution of Net Profit for the accounting period among the partners. |

|

3 |

Nature of Items |

It is debited with the expenses and credited with the income, not being business income to determine net profit for accounting period. |

It is debited with the items of appropriation of profit like salary, commission, interest on capital, transfer to reserve, etc. and credited with the items of income being debited to Partners’ Capital Account or Current Accounts such as interest on drawings. |

|

4 |

Partnership Deed |

This account is not guided by the Partnership Deed or Agreement. |

This account is prepared as guided by the Partnership Deed or Agreement or provisions of Indian Partnership Act, 1932. |

|

5 |

Matching Principle |

It follows the Matching Principle where revenue is matched against expense. |

It does not follow the Matching Principle. |

Application Videos

-

Special Aspects: Salary and Commission ...

This video explains the Meaning and Treatment of Salary and Commission alon...

This video explains the Meaning and Treatment of Salary and Commission alon... -

Meaning and Preparation of Common-Size Statement of Pro ...

This video explains the meaning and preparation of Common-Size Statement of...

This video explains the meaning and preparation of Common-Size Statement of... -

Meaning and Preparation of Common-Size Balance Sheet ...

This video explains the meaning and preparation of Common-Size Balance Shee...

This video explains the meaning and preparation of Common-Size Balance Shee... -

Accounting Treatment of Reserves and Accumulated Profit ...

This video explains the Accounting Treatment of Reserves, Accumulated Profi...

This video explains the Accounting Treatment of Reserves, Accumulated Profi... -

Accounting Treatment of Reserves and Accumulated Profit ...

This video explains the Accounting Treatment of Reserves, Accumulated Profi...

This video explains the Accounting Treatment of Reserves, Accumulated Profi...

Concept Videos

-

Reconstitution: Change in Existing Profit Sharing Ratio ...

Reconstitution: Change in Existing Profit Sharing Ratio, Introduction to Re...

Reconstitution: Change in Existing Profit Sharing Ratio, Introduction to Re... -

Reconstitution: Change in Existing Profit Sharing Ratio ...

Reconstitution: Change in Existing Profit Sharing Ratio, Introduction to Re... -

Reconstitution: Change in Existing Profit Sharing Ratio ...

Reconstitution: Change in Existing Profit Sharing Ratio, Introduction to Re... -

Reconstitution: Change in Existing Profit Sharing Ratio ...

Reconstitution: Change in Existing Profit Sharing Ratio, Introduction to Re... -

Reconstitution: Change in Existing Profit Sharing Ratio ...

Reconstitution: Change in Existing Profit Sharing Ratio, Introduction to Re...